Who Can Actually “Clean” Venezuela’s Dirty Oil?

Heavy crude, sour barrels, and why the winners aren’t producers... they’re refiners.

“Anybody can pull oil out of the ground. The money’s made by the guy who knows what to do with the ugly barrels.”

— Landman

My Uncle always told me that one of the most misunderstood dynamics in global energy markets is the difference between oil quality — and why it matters more than headline production numbers.

You’ll often hear it framed simply:

Venezuela has “dirty oil”

Saudi Arabia has “clean oil”

That shorthand is directionally right.

But the investable insight lives somewhere else entirely.

If Venezuelan supply ever meaningfully returns, the winners won’t be the companies with access to the oil — they’ll be the companies that can process it, upgrade it, and profit from the dirtiest barrels on earth.

While much of the market rushes to buy any oil stock loosely tied to Venezuela, the real opportunity sits downstream, with the firms that own the refining complexity to handle heavy, high-sulfur crude efficiently.

The goal of this post is to unpack that distinction — to explain why oil quality matters, how it reshapes profitability, and why understanding this difference provides an edge that most investors miss.

Because in energy, knowing what kind of oil you’re dealing with often matters more than knowing how much of it there is.

This is not a drilling story.

It’s a refining-asset and infrastructure story.

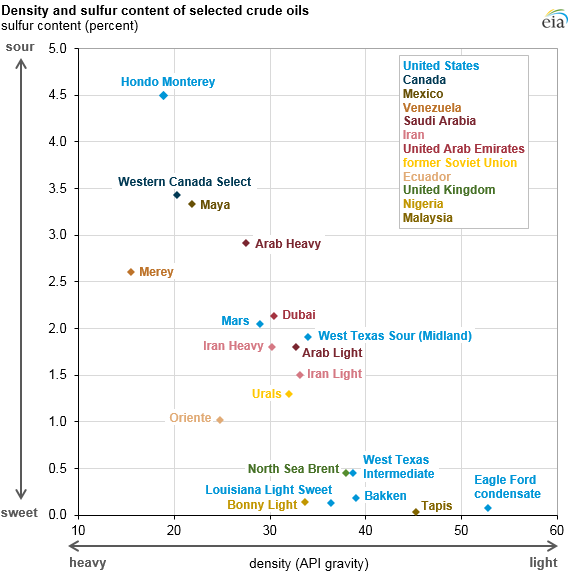

Heavy Sour vs Light Sweet — The Real Divide

Venezuela’s Orinoco Belt crude is among the most extreme feedstocks globally:

API gravity: as low as ~8° (extremely heavy)

Sulfur: very high (“sour”)

Viscosity: requires dilution just to move through pipelines

By comparison, most Saudi grades are:

Medium to light

Lower sulfur

Far easier to refine into finished fuels

Translation:

Venezuelan crude is cheap for a reason. It only becomes valuable in the hands of companies with deep-conversion refining hardware.

The real question isn’t who owns Venezuelan oil — it’s who can clean it up profitably.

The Companies Best Positioned to Handle Venezuela’s “Dirty” Crude

1. Valero Energy VLO 0.00%↑ — The Gold Standard for Dirty Barrels

Valero Energy is arguably the most optimized refiner in the world for heavy sour crude.

Operates complex coking refineries across the U.S. Gulf Coast

Facilities in Port Arthur, Corpus Christi, and Houston were explicitly built to process Venezuelan and Mexican heavy oil

Prior to sanctions, Valero imported ~200,000 barrels/day from PDVSA

Why Valero wins:

Coking units crack low-value residue into diesel, jet fuel, and gasoline

Hydrocrackers and hydrotreaters strip sulfur to meet fuel specs

Heavy crude discounts = margin expansion

In plain English:

Valero turns the dirtiest oil into some of the cleanest profits.

2. Chevron CVX 0.00%↑ — End-to-End Control

Chevron is uniquely positioned because it doesn’t just refine — it controls the chain.

Co-owns upstream JVs with PDVSA

Historically blended Orinoco crude with diluents for export

Processed barrels through the Pascagoula refinery, which can handle medium-to-heavy grades

Why Chevron matters:

Vertical integration allows pre-treatment before refining

Controls blending, logistics, and downstream placement

Less dependent on third-party refiners

Translation:

Chevron doesn’t just clean the oil — it engineers the barrel from wellhead to fuel tank.

Noteworthy: The company pays an attractive 4.17% annual dividend yield.

3. Marathon Petroleum MPC 0.00%↑ & Phillips 66 PSX 0.00%↑ → Built for This, Waiting on Supply

Marathon Petroleum

Phillips 66

Both companies:

Operate deep-conversion coking refineries

Were originally designed for Venezuelan and Canadian heavy crudes

Switched to Canadian WCS after sanctions

Key point:

The hardware already exists. What’s missing is feedstock access.

If Venezuelan barrels re-enter under coordinated policy, these refiners are immediate beneficiaries.

4. Exxon Mobil XOM 0.00%↑ — The Technology Owner

Exxon Mobil no longer operates in Venezuela — but its fingerprints are everywhere.

Built the Cerro Negro upgrader, effectively a mini-refinery

Pioneer in hydrocracking and resid-conversion technology

Lost assets during 2007 expropriations, but retained the IP

Why Exxon still matters:

Engineering expertise sets the industry standard

Technology can be licensed, replicated, or indirectly monetized

Benefits if heavy-oil processing becomes strategically important again

5. European Exposure: ENI, TotalEnergies, Repsol

ENI

TotalEnergies

Repsol

These firms retain:

Smaller JV stakes

Unpaid receivables from PDVSA

Refineries capable of handling heavy blends after dilution

Constraint:

Logistics, sanctions, and political risk cap near-term upside.

6. Saudi Aramco KSA 0.00%↑ — The Benchmark

Saudi Aramco doesn’t need Venezuelan oil — but it could process it!

Motiva Port Arthur refinery is one of the most complex in the world

Massive hydrotreating and desulfurization capacity

Originally designed with heavy-crude flexibility in mind

This highlights the truth: complexity beats purity in refining.

Bottom Line

Valero VLO 0.00%↑ and Chevron CVX 0.00%↑ are the clear front-runners.

Valero: best downstream hardware on earth for dirty oil

Chevron: end-to-end control from wellhead to refinery

Marathon, Phillips 66, and Exxon benefit if trade normalization resumes — they already own the steel and the science.

European exposure exists, but it’s secondary.

Strategic Implication

If Venezuelan heavy crude re-enters global markets under U.S. coordination, the winners are not producers.

They are:

Complex refiners

Integrated majors

Owners of coking and hydroprocessing capacity

This is a refining-asset trade — not a production-volume trade.

And that distinction is where the edge lives.

Disclaimer: For informational and educational purposes only, not investment advice or a recommendation to buy or sell any securities.