The Thaw - #2

How Semiconductors Become the First Great Winners of the Credit Super-Cycle

As I mentioned before, we are living through the greatest credit expansion of our generation, and it doesn’t have a name yet. I’m calling it The Thaw.

The name captures what came before: the deepest freeze in modern monetary history. Between March 2022 and July 2023, the Federal Reserve (FED) executed the most aggressive tightening cycle in four decades — 525 basis points in 16 months. Capital markets seized. Regional banks failed. The yield curve inverted deeper than any point since Volcker. Money, for the first time in a generation, had a real cost.

And then it didn’t break.

That’s what makes The Thaw historic. Every prior tightening cycle of this magnitude ended in recession, deleveraging, and forced liquidation. This time, the ice held just long enough — and now it’s melting.

What we’re witnessing is the controlled release of trillions in sidelined capital. Money market funds sit at record highs → $ 7.53 trillion. Corporate balance sheets survived intact. The labor market never cracked. And now, with the Fed pivoting toward cuts while deficit spending runs at wartime levels and AI capex creates a new infrastructure super-cycle, the conditions exist for a credit expansion unlike anything we’ve seen since the post-2008 QE (Quantitative Easing) era — perhaps larger.

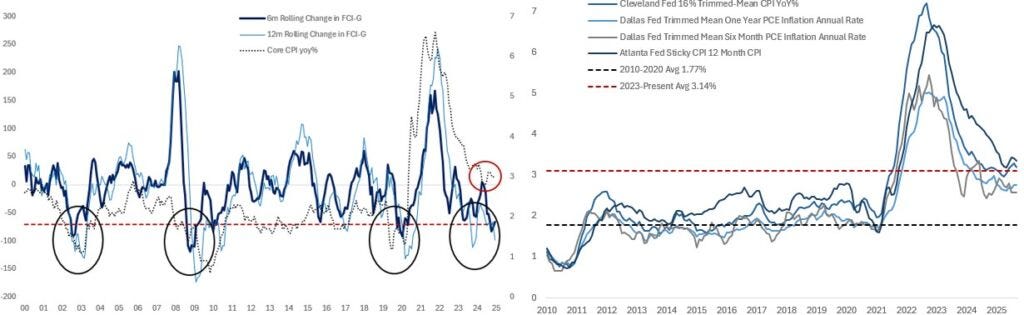

Even Citadel Securities — one of the most data-driven Macro desks on earth — is pointing to the same shift.

In their recent note Giving Thanks to Monetary Policy, they show that financial conditions have eased sharply, liquidity is improving, and both duration and credit are being aggressively bought again. The freeze is cracking in real time.

The Thaw isn’t a boom. It’s not a bubble. It’s the slow, inexorable return of liquidity to a system that was frozen but never truly broken. Capital is flowing again — into risk assets, into credit markets, into the real economy.

The freeze satisfied nothing.

The Thaw inherits everything.

Why The Thaw Starts With Chips

If you want to see where a credit expansion actually shows up first, you don’t start with headlines or GDP prints. You start with capex — who is spending, on what, and how heavily they rely on financing to do it. (Capex = Capital Expenditure)

In this cycle, one sector sits dead center:

Semiconductors are the backbone of The Thaw.

Every big structural theme plugs into chips:

AI and large language models (LLMs)

Cloud and hyperscale data centers

Edge computing and 5G

Autonomous vehicles and industrial automation

Defense, drones, and autonomy

Consumer electronics and gaming

Energy, grid, and smart infrastructure

If credit is the bloodstream of this cycle, semis are the organs that get fed first.

From Freeze to Fire: How AI Turned Chips Into a Credit Sponge

During the tightening cycle, the Fed tried to cool risk by raising the cost of capital. But something strange happened: AI demand didn’t care.

Hyperscalers kept spending on GPUs and accelerators.

Semiconductor equipment orders dipped, but the long-term capex plans didn’t disappear.

Every big tech CEO started talking about “AI infrastructure” like it was a matter of national security.

The result? The freeze hit housing, small businesses, and speculative growth stocks harder than it hit the core of the compute build-out.

Now, as rates drift lower and credit loosens, the sector that never really stopped is positioned to accelerate.

The Thaw doesn’t create semiconductor demand from scratch.

It releases demand that was already there — and now can be financed more aggressively.

The Semiconductor Stack: Where the Credit Actually Flows

When people say “chips,” they think Nvidia and maybe AMD. From a credit perspective, the reality is much bigger and more layered.

Think of the semi ecosystem as a capital stack:

1. GPU & Accelerator Giants (AI Compute Layer)

These are the names everyone knows because they sit at the top of the AI narrative:

High-end GPUs and accelerators for training and inference

Networking, interconnects, and custom AI systems (DGX, etc.)

Software stacks that lock in customers for years

These companies are the first call on AI capex. When hyperscalers raise debt or redirect free cash flow toward AI, the order book for this layer explodes.

In a credit expansion, this group benefits from:

Larger, longer-duration capex commitments

Customers more willing to over-order capacity

New verticals (defense, auto, healthcare) joining the AI arms race

2. Foundries & Advanced Manufacturing (The Fabs)

This is where The Thaw becomes truly credit-intensive.

Leading-edge fabs are trillion-dollar national projects spread over years:

3 nm, 2 nm, and below require insane upfront investment

Clean rooms, lithography, EUV machines, power, water, logistics

Government subsidies blended with corporate balance sheets and debt issuance

Even modest changes in financing conditions can shift timelines:

Lower rates → more projects that clear the hurdle

Tighter spreads → larger, more ambitious fab roadmaps

Friendly policy → sovereign + corporate capital crowds in

In The Thaw, fabs are where policy, credit, and technology collide.

3. Semi Equipment & Tools (Picks and Shovels)

If fabs are castles, equipment makers are the companies that sell the bricks and blueprints.

This layer benefits from:

Every incremental fab project

Every capacity expansion announcement

Every node shrink and technology transition

The beauty of this group in a credit expansion:

They don’t need to bet on which GPU wins the AI war.

As long as “more wafers, more layers, more complexity” is the direction of travel, their order books stay fat.

4. Materials, Packaging, and Memory (The Plumbing)

At the bottom of the stack:

HBM memory

Advanced substrates and packaging

Specialty chemicals, gases, and deposition materials

Copper, aluminum, rare gases, and other metals that make fabs possible

This stuff is not sexy. It is essential.

The more credit flows into fabs and AI infrastructure, the more these companies see multiyear demand visibility — which they then lever into their own:

Capacity expansions

M&A

Long-term supply agreements

In other words: credit expansion at the top of the stack cascades down the entire chain.

Why Semis Are the “Railroads” of This Cycle

In previous eras:

Railroads were the backbone of the 19th-century credit booms

Highways and autos anchored mid-20th-century expansions

The internet build-out defined the late-90s capex wave

Today, semiconductors are the new critical infrastructure.

A few key reasons:

They’re upstream of everything.

AI, cloud, defense, EVs, grid modernization — all of it consumes more silicon.They’re globally strategic.

Governments are treating chips like oil. That means subsidies, cheap financing, and political will.They’re insanely capital-intensive.

You don’t “lightly” invest in a fab. You commit tens of billions and then spend the next decade executing.They’re naturally leveraged to credit conditions.

Better financing terms → more projects → fatter order books → stronger earnings → higher equity multiples.

In The Thaw, when liquidity returns and credit conditions ease, semis feel it first and most forcefully.

How The Thaw Changes the Semi Cycle

Historically, semis have been brutally cyclical:

Overbuild → inventory glut → price collapse → capex cuts → repeat.

The Thaw doesn’t magically remove cyclicality, but it does mutate it.

Here’s how:

More Structural Demand, Less Purely Consumer-Driven

A larger share of demand is now tied to:

Data centers and AI clusters

Industrial and defense applications

Long-dated government or hyperscaler projects

These buyers don’t behave like a gamer deciding to skip a GPU upgrade. They plan 3–10 years out and finance accordingly.

More Policy Backstops

When fabs are wrapped in:

Subsidy packages

Tax incentives

“National security” language

The odds of brutal, uncontrolled capex collapses go down. Politicians don’t like shuttered mega-projects.

Private + Public Credit Blending

The next leg of the cycle will be financed by a mix of:

Corporate bonds and loans (We’ve seen Google issue debt “bonds” this year)

Government grants and guarantees

Sovereign wealth funds

Private credit and infrastructure funds

That blend matters. The more diversified the capital base, the more resilient the build-out.

The result?

The semi cycle will still have drawdowns, but each trough (bottom) starts from a higher floor and resets into a larger total addressable market.

Where the Equity Optionality Lives

This is not investment advice, but if you think The Thaw is real, you naturally end up mapping it into exposure buckets.

From a framework perspective (not a recommendation list), The Thaw’s semi complex breaks into:

1. AI Compute Leaders

These are the companies at the top of the AI capex chain — the names that get paid every time a hyperscaler builds a new cluster or an enterprise adopts AI internally.

NVIDIA (NVDA) — Dominant in AI training with H100/H200 and the upcoming Blackwell platform.

Advanced Micro Devices (AMD) — MI300 accelerators for training and inference.

Broadcom (AVGO) — Custom accelerators and networking silicon for cloud providers.

Intel (INTC) — Xeon + Gaudi for inference and mixed AI workloads.

Arm Holdings (ARM) — Instruction set architecture powering edge and cloud AI designs.

Marvell Technology (MRVL) — Custom ASICs and AI-optimized networking processors.

Why they matter:

These companies monetize every incremental dollar of AI spending. When credit loosens and capex accelerates, this group sees demand first.

2. Foundries & IDMs

This layer physically manufactures the silicon — and its capex cycles move almost one-to-one with global liquidity and industrial policy.

TSMC (TSM) — The world’s leading foundry; the backbone of Apple, NVIDIA, AMD.

Samsung Electronics — Advanced foundry + memory integration.

Intel (INTC) — IDM 2.0 strategy to serve external foundry customers.

Why they matter:

Foundry expansion is credit-intensive. When financing costs fall, nodes shrink, and megaprojects move forward.

3. Equipment & Tools (Picks and Shovels)

The companies that supply the equipment used to build every fab on earth.

ASML (ASML) — Exclusive provider of EUV lithography tools.

Applied Materials (AMAT) — Broad process equipment across logic and memory.

Lam Research (LRCX) — Etch and deposition tools for advanced nodes.

KLA (KLAC) — Yield management and metrology — critical for scaling nodes.

Why they matter:

Equipment makers monetize every fab project worldwide. Their order books stretch years when credit flows.

4. Memory, Packaging & Materials

The plumbing of the AI era — the behind-the-scenes capacity that determines how far compute can scale.

Micron (MU) — Leader in HBM3/HBM4 for AI accelerators.

SK hynix — Major supplier of high-bandwidth memory to NVIDIA.

Samsung Electronics — Largest memory producer globally.

Why they matter:

AI compute is becoming packaging-constrained and memory-constrained. This group is levered to density, not hype.

If the greatest credit expansion of our time is just getting started, this is the part of the market that sees the checks first — from hyperscalers, sovereigns, corporates, and governments. These businesses are not cyclical gadgets; they are the infrastructure of the next decade.

What Could Break This?

Every macro thesis needs a kill switch.

For The Thaw’s semi leg, the key risks look something like:

Policy shock – sudden reversal on subsidies, trade restrictions that distort supply chains, or geopolitical escalation that disrupts fabs.

Demand disappointment – AI monetization lags, enterprises slow adoption, or models become more compute-efficient faster than expected.

Funding squeeze – a second, unexpected tightening cycle or inflation spike that forces central banks back into “hammer mode.”

None of these are impossible. But until one of them appears in the data, the base case is simple:

Credit is becoming cheaper at the same time that

Structural demand for compute is exploding, and

Governments are underwriting strategic capex with policy and subsidies.

That’s the kind of alignment you don’t see often.

The Thaw, Chapter Two

In the first post, I laid out the big picture: we’re at the beginning of the greatest credit expansion of our era.

The Thaw is what it feels like on the ground:

Money that survived the freeze is now looking for a home.

AI and reshoring have turned semiconductors into critical infrastructure.

Credit, policy, and technology are converging on one sector in a way we haven’t seen since railroads, highways, or the early internet.

This isn’t about guessing the next quarter’s earnings beat.

It’s about recognizing that when liquidity returns, it doesn’t spread evenly.

It finds:

Capital-intensive projects

Strategic assets

Systems the world can’t function without

Right now, semis sit at the intersection of all three.

We are still early.

The ice is just starting to crack.

Most people are still arguing about whether AI is “overhyped.”

Meanwhile, the credit pipes are warming, fabs are being announced, and balance sheets are quietly rearranging themselves around one idea:

More compute, everywhere, all at once.

That’s The Thaw.

And this is just one chapter.

In the next installments of this series, I’ll break down the other pillars of the credit expansion — metals, energy infrastructure, and the emerging markets that get pulled into this super-cycle.

For now, remember:

Credit waves don’t ring a bell at the start.

They build in the plumbing first.

Semis are the plumbing.

Welcome to Chapter Two.