The Platinum Flywheel: Why Jensen, Leopold, and Jane Street Are All Betting on the Same Stock

CoreWeave (CRWV): The landlord of the intelligence economy

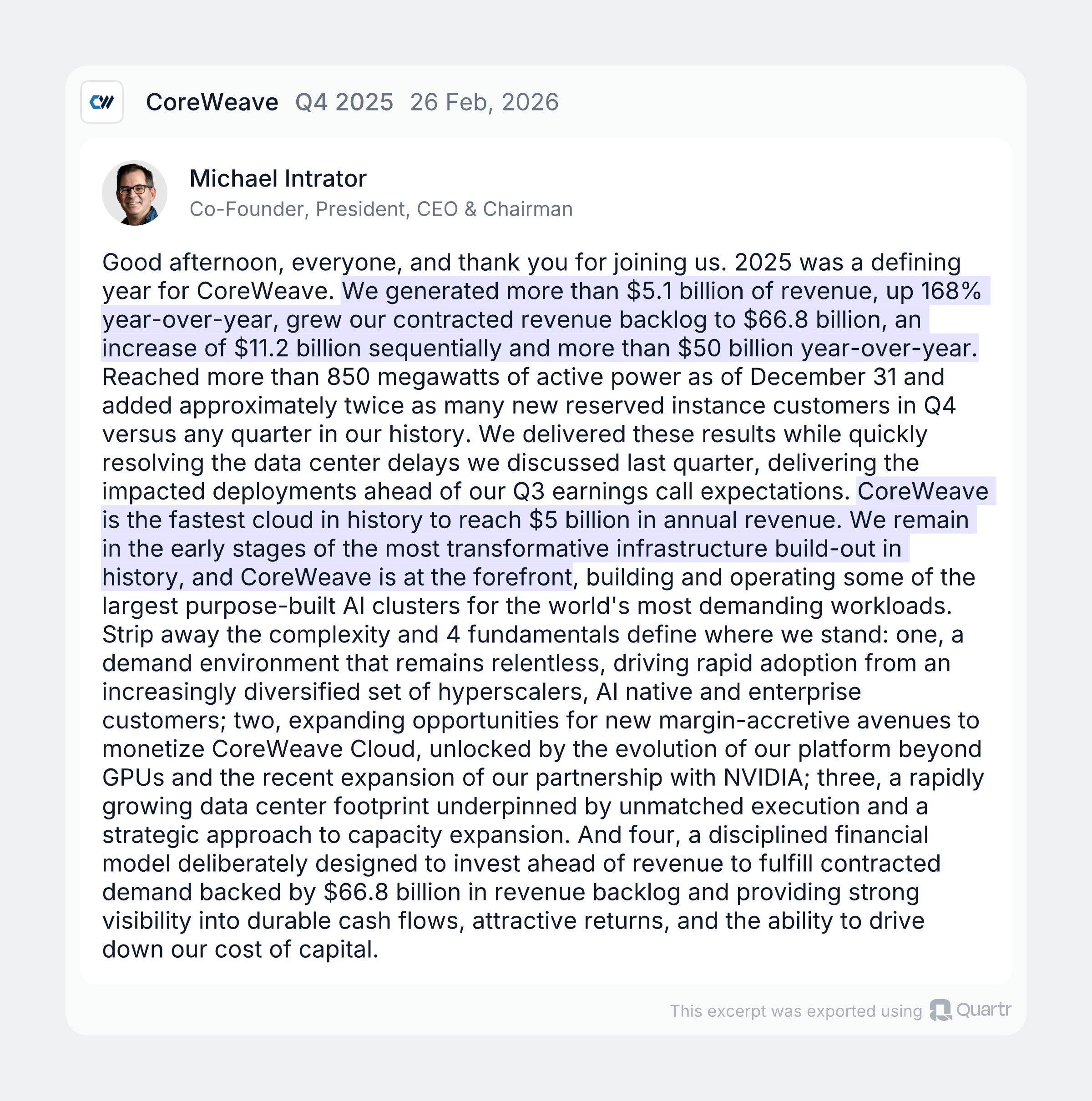

$5.1 billion in revenue. $66.8 billion in backlog. The fastest cloud in history to $5B. And the smartest money in the world — Jensen Huang, Leopold Aschenbrenner, Jane Street — is still buying.

Rome had aqueducts. The AI era has CoreWeave.

— LRMI, November 2025

Time for my thesis for CoreWeave CRWV 0.00%↑

The Smartest Money in the World Just Showed Its Hand

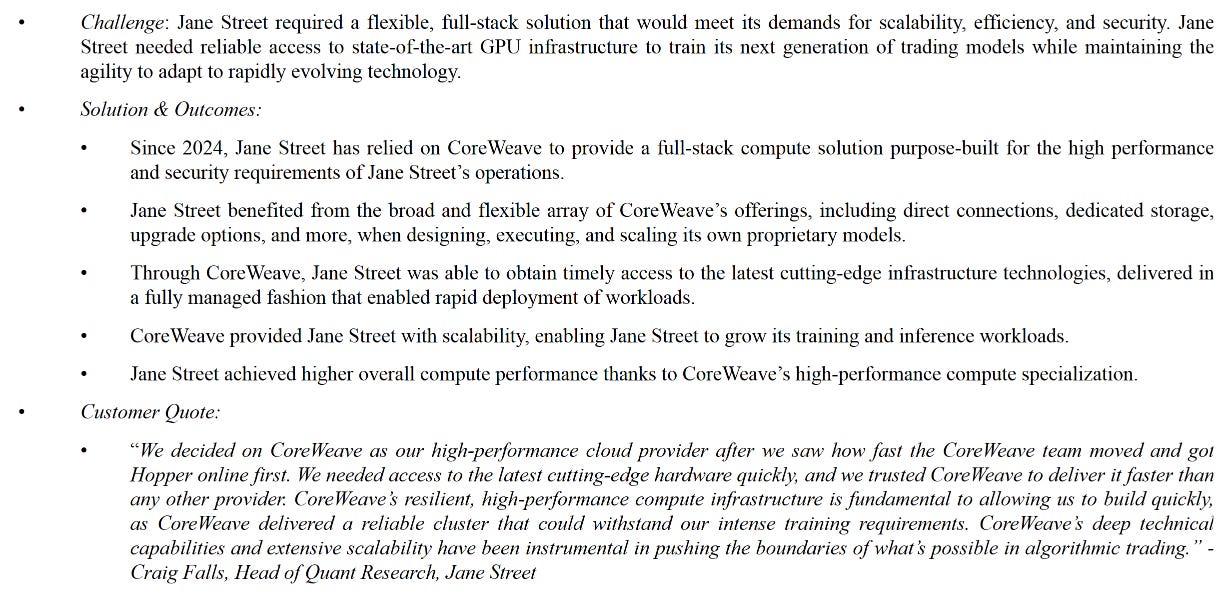

This week, Jane Street — a global quantitative trading firm that handles billions in daily volume and operates with arguably the strictest security and performance requirements of any financial institution — committed approximately $6 billion to use CoreWeave’s AI cloud platform. On top of that, Jane Street made a $1 billion equity investment in CoreWeave Class A common stock at a purchase price of $109.00 per share. Article Link

Let that sink in. The most mathematically rigorous firm in finance didn’t just rent GPUs. They bought a billion dollars of the stock. At $109.

Under the expanded agreement, CoreWeave will provide Jane Street with next-generation compute across multiple facilities, including access to NVIDIA’s Vera Rubin architecture and the full software and services stack required to deploy and scale AI at the frontier of quantitative research. CoreWeave was selected for its ability to combine high-performance compute with an integrated software layer that operates efficiently and consistently under real-world conditions — with dedicated connectivity, custom storage configurations, and responsive technical support tailored to Jane Street’s research operations.

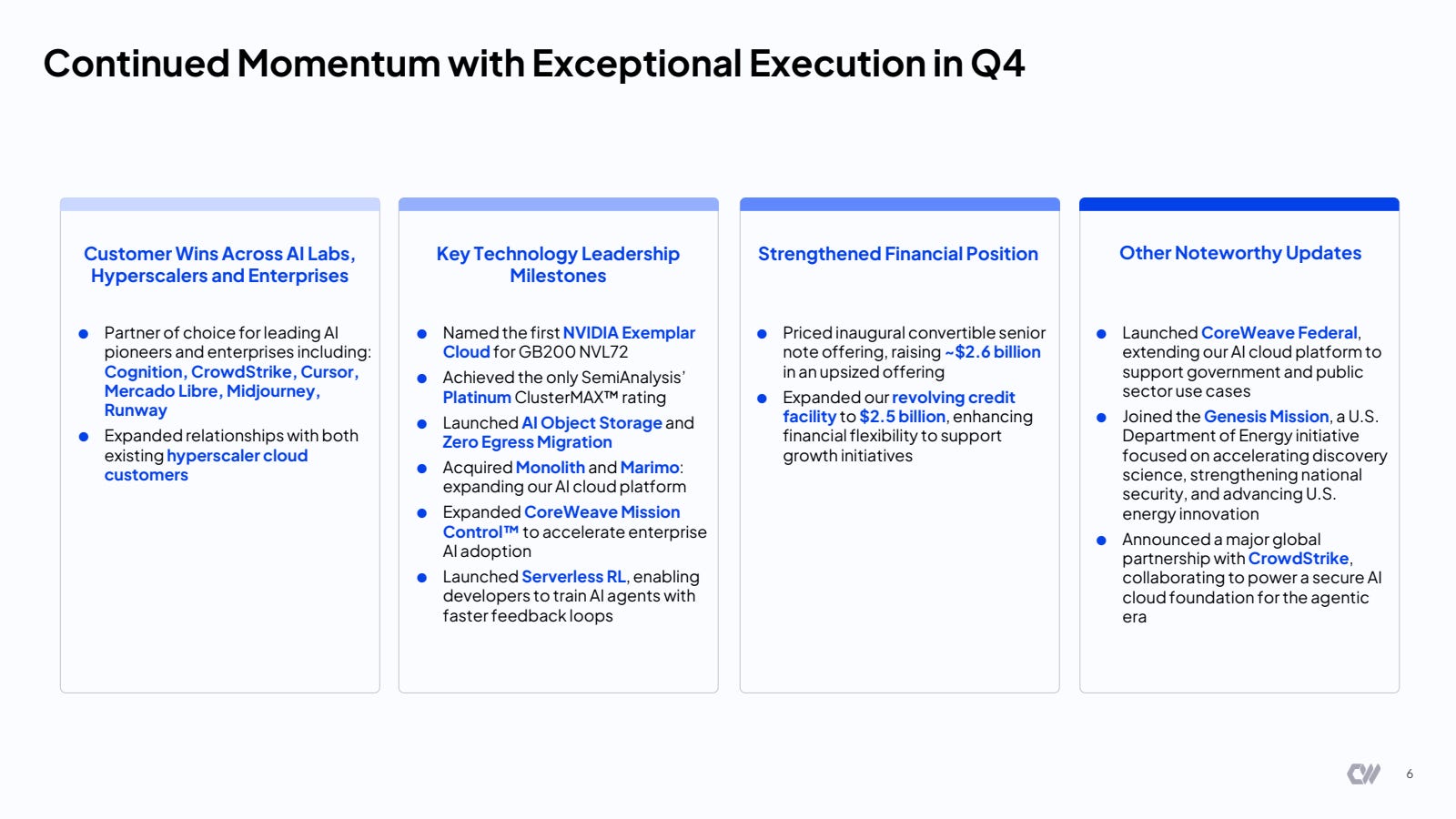

This isn’t a press release you skim. This is a signal you study. Jane Street joins NVDA 0.00%↑ NVIDIA, META 0.00%↑ Meta, Anthropic, and OpenAI in placing multi-billion-dollar, multi-year bets on CoreWeave as the essential infrastructure layer for AI. The contract backlog now includes $21B from Meta (through 2032), $6.3B from NVIDIA (capacity backstop through 2032), a multi-year agreement with Anthropic (announced April 10), and now $6B from Jane Street — over $33 billion in committed or contracted demand from four of the most sophisticated capital allocators on the planet.

The question every investor should be asking: what do they know that the market doesn’t?

The Rating That Started It All

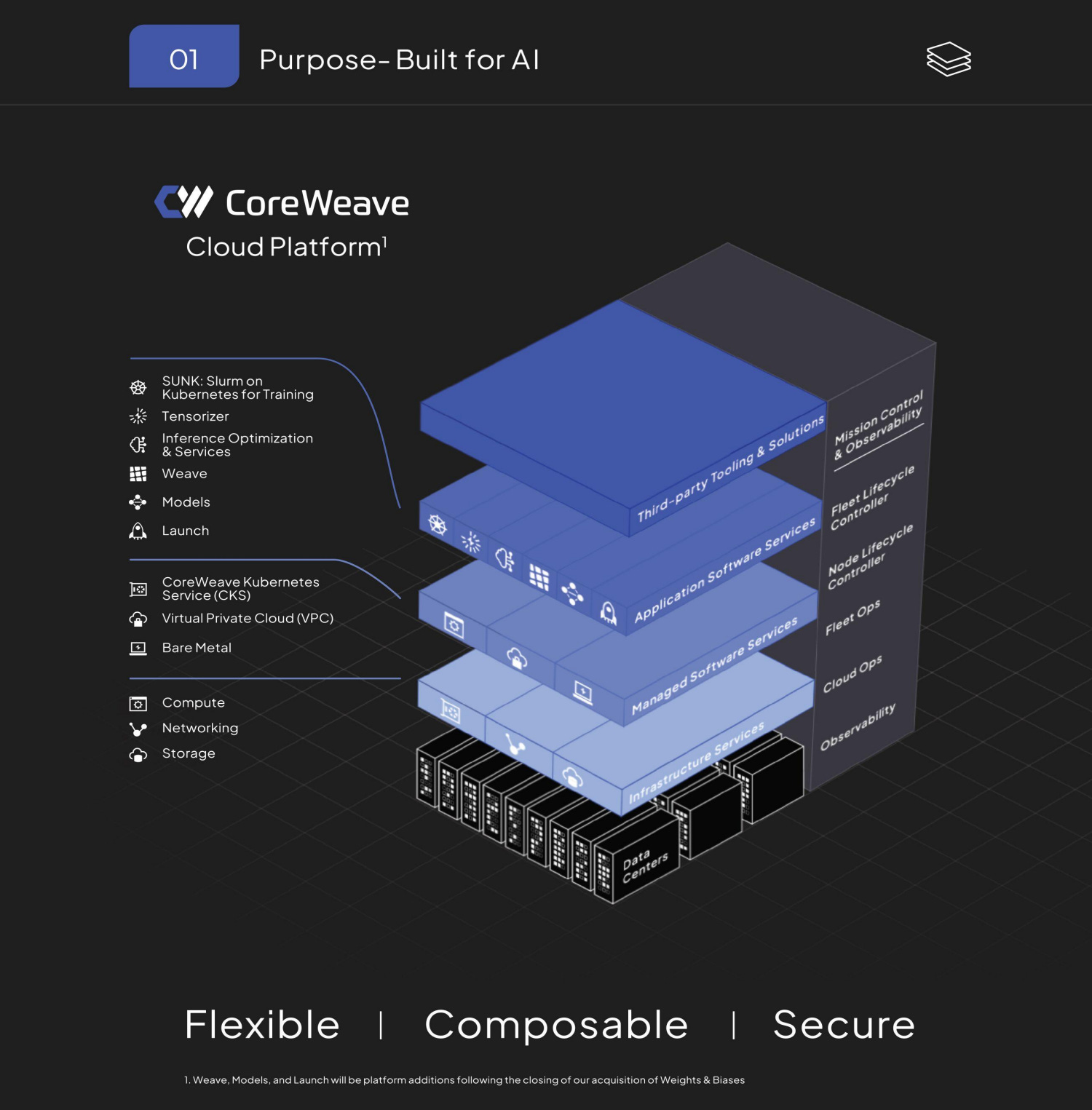

To understand why this caliber of customer keeps choosing CoreWeave, you have to understand the SemiAnalysis ClusterMAX™ Rating System — the closest thing the neocloud industry has to a Moody’s-style credit rating, but for GPU cloud performance.

SemiAnalysis (founded and run by Dylan Patel) is the most respected independent semiconductor and AI infrastructure research shop in the space. Their ClusterMAX system independently tested dozens of GPU clouds covering approximately 90% of the entire GPU rental market by volume, evaluating providers from the perspective of a typical enterprise customer across five tiers: Platinum, Gold, Silver, Bronze, and UnderPerform. ClusterMAX 2.0, released in November 2025, reviewed 84 providers across a market map of 209 total companies, incorporating interviews with over 140 end users.

CoreWeave is the only AI cloud provider to achieve the Platinum rating. Twice. No other provider came close — to reach Platinum, a provider needs to score 90+ out of 100 in nearly every category with almost no weak points. The full tier breakdown tells the competitive story clearly:

Platinum: CRWV 0.00%↑ CoreWeave (sole provider)

Gold: NBIS 0.00%↑ Nebius, ORCL 0.00%↑ Oracle, MSFT 0.00%↑ Azure, Crusoe, Fluidstack

Silver: GOOG 0.00%↑ Google Cloud, AMZN 0.00%↑ AWS, Together.ai, Lambda

Bronze: DataCrunch, TensorWave, and others

AWS is Silver. Google Cloud is Silver. Azure is Gold. CoreWeave stands alone at the top.

What SemiAnalysis Actually Tested

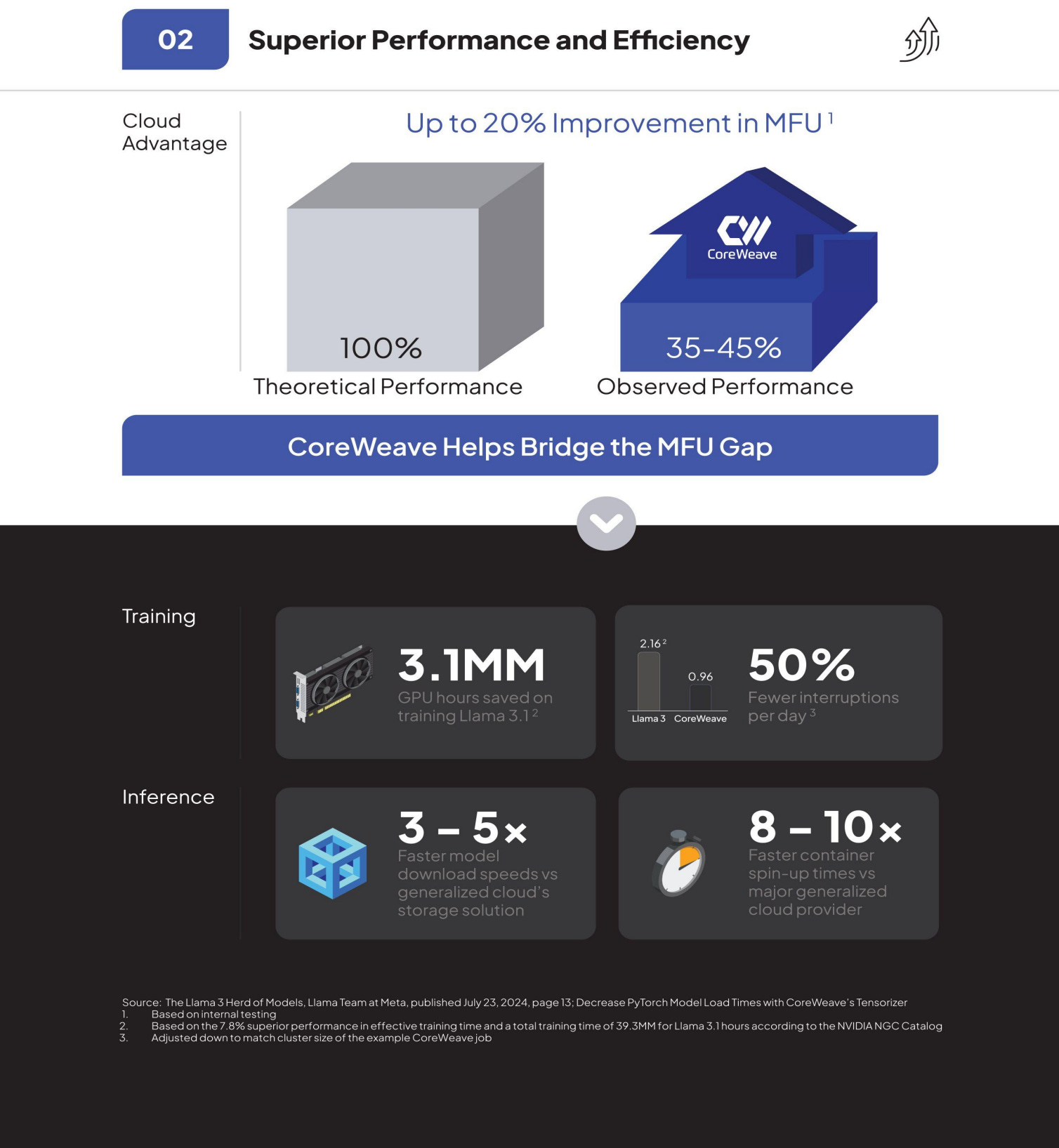

The benchmarking wasn’t a survey or a questionnaire. SemiAnalysis ran a year-long series of tests spanning single-node setups to massive 1,000+ GPU clusters, evaluating ten criteria including security, storage, orchestration, reliability, networking performance, technical expertise, and pricing.

Some concrete results from ClusterMAX 2.0: on the PyTorch install test (a proxy for WAN connection quality and local disk I/O), CoreWeave completed the install in roughly 3.2 seconds versus a median of 8.5 seconds across all providers — and a staggering 41.2 seconds for one Bronze-tier provider. On the 22.1GB NGC container pull test, CoreWeave completed it in under 10 seconds (they maintain local NGC mirrors), while Gold-tier providers took 45-60 seconds.

But the benchmarks that matter most for the investment thesis are the ones that translate directly into dollars.

The Six Competitive Advantages That Create the Flywheel

1. Goodput & Reliability — The Cash Generation Engine

CoreWeave’s Mission Control platform delivers 50% fewer job interruptions when running GPU clusters of over 1,000 nodes, achieving a goodput rate as high as 96% versus the industry average of 90%.

This is the single most important number in the entire neocloud economy. On a 10,000-GPU training run at $2.35/GPU/hr, that 6-percentage-point delta means roughly $12.3 million in saved compute per year per cluster. CoreWeave operates 250,000+ GPUs — the aggregate efficiency advantage is worth hundreds of millions annually to its customers. This is why they keep coming back, and why they sign multi-year deals worth billions.

2. Pricing Power — The Platinum Premium

SemiAnalysis validated that Platinum-tier providers command a pricing premium over competitors because the total cost of ownership is better, even when the raw $/GPU-hr is higher on paper. CoreWeave is the only cloud to consistently command premium pricing across SemiAnalysis’s interviews with 140+ end users.

This isn’t a vanity award. It’s a validated pricing moat.

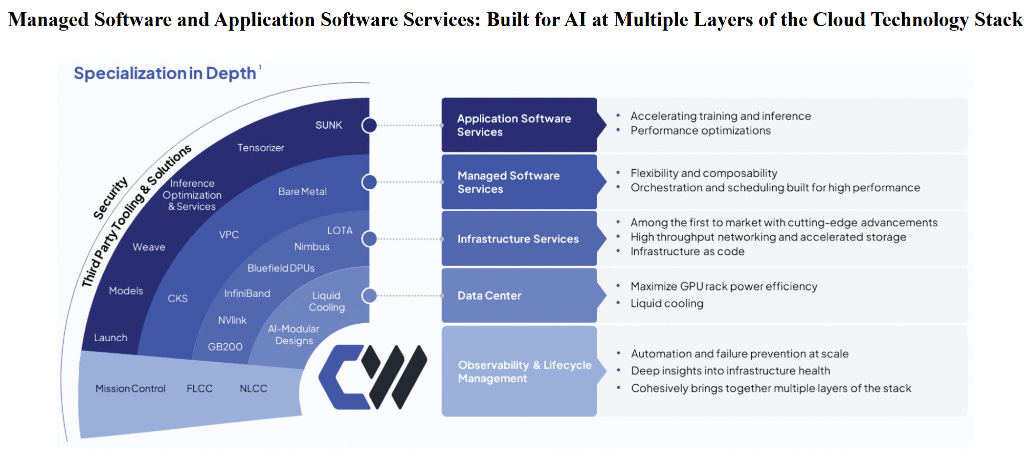

3. Storage Innovation — CAIOS & LOTA

CoreWeave’s proprietary AI Object Storage (CAIOS) and Local Object Transfer Accelerator (LOTA) were rated industry-leading by SemiAnalysis. LOTA transparently caches data on compute node local drives, eliminating storage bottlenecks that can represent over 20% of cluster TCO for data-heavy workloads like video generation, weather prediction, drug discovery, and robotics.

4. Orchestration — SUNK & CKS

SemiAnalysis recognized CoreWeave’s Slurm on Kubernetes (SUNK) and CoreWeave Kubernetes Service (CKS) as best-in-class for managing distributed AI workloads. The validation that matters: even Meta and Jane Street — organizations with world-class internal engineering — choose CoreWeave’s managed orchestration rather than building their own.

5. Security — The Enterprise Moat

SemiAnalysis specifically highlighted CoreWeave’s GPU/InfiniBand-specific pentesting, VPC isolation, and real-time threat detection as industry-leading. This matters because enterprises rarely rent from emerging neoclouds — they gravitate toward CoreWeave because it has crossed the security hurdle that blocks every other neocloud from enterprise adoption. Jane Street, with arguably the strictest security requirements of any firm in the world, chose CoreWeave. That’s the ultimate security certification.

6. Customer Entrenchment

SemiAnalysis concluded that CoreWeave is entrusted to manage the large-scale GPU infrastructure for AGI labs like OpenAI, high-frequency trading firms like Jane Street, and even NVIDIA’s internal clusters. Read that again — NVIDIA trusts CoreWeave to run its own compute.

The Internal Pitch: What CoreWeave Showed Jensen

Jensen Huang’s exact words on CNBC: “We’re always looking for great startups to invest in. One of my favorite ones was CoreWeave... My only regret is I didn’t invest enough.”

I think the surface-level narrative — “of course he loves them, they buy his chips” is a lazy analysis. NVIDIA’s 13F shows CoreWeave as its largest equity investment by far: over 24 million shares worth $3.2+ billion, representing more than 90% of NVIDIA’s entire reported equity portfolio. NVIDIA increased its stake from 17.9 million shares at IPO to 24.28 million shares during Q2 2025.

Jensen isn’t diversifying. He’s building a vertically integrated AI ecosystem. Here’s what was really on the pitch deck:

The Capacity Backstop — A Zero-Downside Floor

CoreWeave entered a $6.3 billion agreement where NVIDIA is obligated to purchase any unused cloud capacity through April 2032. The mechanic is elegant:

NVIDIA sells GPUs to CoreWeave → revenue for NVIDIA

CoreWeave rents them at premium pricing → revenue for CoreWeave

If demand softens → NVIDIA buys the residual capacity → CoreWeave still generates revenue

NVIDIA uses that capacity for internal R&D or partner allocations → NVIDIA gets utility

CoreWeave effectively holds a put option on its own inventory, written by the strongest balance sheet in the semiconductor industry. This crushes CoreWeave’s cost of capital — the single biggest variable in neocloud economics — because lenders know NVIDIA is backstopping billions in demand.

Jensen didn’t invest in a customer. He built a demand-guaranteed distribution channel for his own silicon.

The AWS Playbook on GPUs

The pitch wasn’t “we rack and stack GPUs.” It was: “We’ve built a proprietary software stack that makes GPU compute actually work at scale.” Jensen recognized this as the AWS playbook replayed on accelerated compute — the infrastructure layer becomes the moat, not the hardware.

Scale Economics

CEO Mike Intrator said the quiet part out loud: “If we stop growing at the rate we’re growing, this company would become enormously profitable within three months. We’re making the strategic decision to get to scale.”

The cost structure is almost entirely fixed — capex-funded GPUs, datacenter leases, networking. Once you cross the utilization threshold, every marginal dollar of revenue falls to the bottom line at 60-80% incremental margins. Revenue guidance: $5B to $12B+ by end of 2026. The GPU pricing environment validates the model — H100 1-year rental pricing surged almost 40% from $1.70/hr in October 2025 to $2.35/hr by March 2026, and on-demand capacity is completely sold out.

The Variant Perception: What Leopold, Jensen, and Jane Street Know

Leopold Aschenbrenner’s Situational Awareness fund — the $1.5B+ AGI-focused hedge fund backed by the Collison brothers, Daniel Gross, and Nat Friedman — has made CoreWeave one of its highest-conviction positions. In Q4 2025, the fund added 9.4 million shares of CoreWeave call options, a 672% increase in position size. The fund’s total US equity and options portfolio expanded from $254 million in Q4 2024 to over $5.5 billion by Q4 2025, with CoreWeave as a top holding.

Leopold exited NVDA and AVGO in Q4 2025 and rotated aggressively into the physical infrastructure layer — CoreWeave, Core Scientific, Applied Digital, Bloom Energy, Solaris Energy, and Bitcoin miners pivoting to AI hosting. His thesis: the bottleneck in the race to AGI has shifted from chips to power, cooling, and physical data center capacity. CoreWeave is the operator that converts that physical infrastructure into revenue-generating compute.

The variant perceptions that Jensen, Leopold, and now Jane Street are all pricing in:

1. CoreWeave is a compute utility, not a GPU rental company. GPU rental implies commodity, low-margin, replaceable. Compute utility implies recurring revenue, switching costs, pricing power, and operating leverage. The Platinum rating proves it. You don’t call AWS a “server rental company.”

2. The debt is a feature, not a bug. The market sees $13B+ in debt and panics. The smart money sees an asset-backed lending structure where every dollar of debt is secured by physical GPUs with contracted cash flows — backstopped by NVIDIA through 2032. The cost of capital compresses as CoreWeave scales, which is exactly what Intrator described.

3. The GPU shortage is structural, not cyclical. SemiAnalysis identified a massive disconnect between tightening supply dynamics on the ground (40% pricing surge, sold-out on-demand capacity) and bearish public market sentiment still anchored to narratives of eventual oversupply. The reality on the ground points to sustained scarcity and pricing power.

4. The inference transition creates a second S-curve. Most of CoreWeave’s revenue today is training workloads. But inference — running models in production — is a much larger TAM, more recurring, and more latency-sensitive, which means the quality premium that justifies Platinum pricing gets even wider. CoreWeave holds a leading 20% share of the neocloud market and is positioned as a primary beneficiary of this transition.

5. Jane Street’s $1B equity buy at $109 is the ultimate validation. This isn’t a strategic partnership disguised as investment. Jane Street runs quantitative models on everything. They modeled CoreWeave’s unit economics, stress-tested the balance sheet, analyzed competitive positioning, and put a billion dollars of their own capital on the line at $109. When the most mathematically sophisticated firm in finance — a firm that literally makes markets for a living — buys equity alongside Jensen Huang and Leopold Aschenbrenner, the signal-to-noise ratio is deafening.

The Bear Case (and Why It’s Getting Weaker)

Every honest thesis addresses the risks. The bears have three arguments:

“The hyperscalers will catch up.” Maybe. But SemiAnalysis has evaluated them twice, and AWS is Silver, Google is Silver, Azure is Gold. CoreWeave has been Platinum both times. The gap isn’t closing — it’s widening on dimensions like storage (CAIOS/LOTA), orchestration (SUNK/CKS), and security.

“The debt is unsustainable.” It would be, without contracted demand. But $33B+ in committed revenue from Meta, NVIDIA, Jane Street, and Anthropic — plus 96% utilization and rising GPU pricing — transforms the debt from existential risk into leveraged upside. Every dollar of debt is matched by a GPU generating contracted cash flow.

“GPU prices will collapse.” SemiAnalysis data says the opposite is happening right now. H100 rental pricing surged 40% in six months. On-demand is sold out. The shortage is structural, driven by the inference transition and hyperscaler capex acceleration (Goldman projects $432B in hyperscaler spending in 2026).

The Pitch Deck Jensen Saw (Reconstructed)

If I had to guess the five slides that helped CoreWeave close the deal with Jensen Huang:

“We run your chips better than anyone in the world.” 96% goodput, Platinum rating, trusted by OpenAI + Jane Street + NVIDIA itself.

“The flywheel: your backstop de-risks our capex, which de-risks your channel.” The circular economics of the $6.3B capacity agreement.

“We’re building the AWS of AI before anyone else gets to scale.” First-mover on GB200/GB300 deployment, SUNK orchestration, Mission Control.

“The unit economics at scale are 60%+ incremental margins.” Operating leverage from fixed-cost infrastructure with rising utilization and pricing.

“The TAM is every AI model that will ever run in production.” The inference transition multiplies the addressable market by 10x.

Jensen didn’t invest in a GPU buyer. He invested in the distribution layer that makes his entire ecosystem work. CoreWeave is to NVIDIA what AWS was to Intel in 2006 — except this time, the chip company owns equity in the cloud.

Bottom Line

The market sees a levered, unprofitable GPU rental shop. Myself, Jensen Huang, Leopold Aschenbrenner, and Jane Street see the essential infrastructure utility for the most important technology buildout in human history — with contractually guaranteed demand, pricing power validated by independent testing, a $33B+ contract backlog, and a path to enormous profitability that management says is three months away if they just stopped growing.

They’re not stopping.

Disclaimer: This is not financial advice. Do your own research before purchasing securities

I recently revisited Leopold’s 2024 Situational Awareness essay and ranked each prediction against reality. I also spent time looking at his career, worldview, and the evolution of his fund through its 13F filings since Q4 2024. Put it all into a piece I think you’d enjoy. Check it out on my profile