The Korea Discount Is Closing. Here's My Basket.

Why I'm buying 15 Korean equities with personal capital, and what changed in 2026 that makes this trade structurally different from every prior "Korea is cheap" pitch.

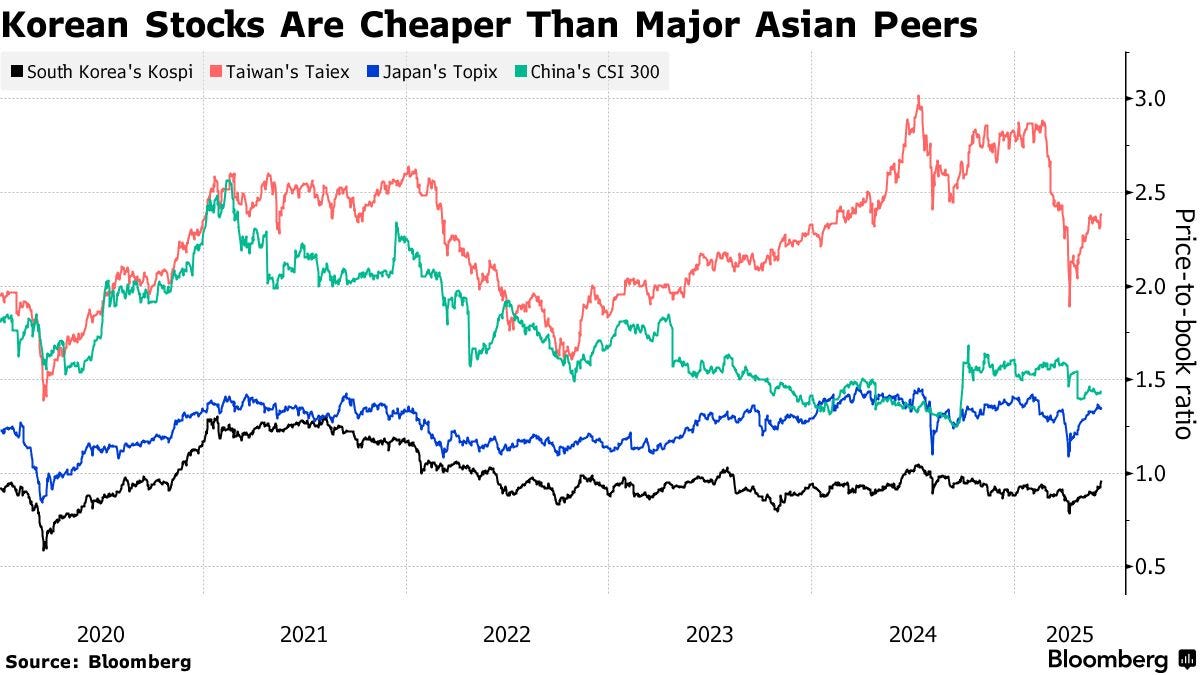

For 25 years, “Korea is cheap” has been one of the worst trades in global equities. Every cycle, some value manager rediscovers that KOSPI trades at half the price-to-book of the S&P 500. Every cycle, the discount persists. Every cycle, the same explanation: chaebol governance is broken, controlling families extract value from minority shareholders, retail gets churned, foreign capital stays underweight.

The discount was rational. Korean corporate law genuinely did not protect minority shareholders. Directors owed fiduciary duty to “the company,” which in practice meant the controlling family. Treasury stock was used as a financial engineering tool to entrench control. Mergers happened at unfair ratios. Cross-shareholdings hid value. The market priced this correctly. The Korea Discount was not a mispricing, it was an accurate read on the legal architecture.

What changed in late 2025-2026 is that the legal architecture changed.

The regime change

On July 22, 2025, an amendment to Article 382-3 of the Korean Commercial Code took effect. It explicitly extends director duty of loyalty to shareholders, not solely to the company. The vote was 220 to 272 — not symbolic, statutory. On August 25, 2025, a second amendment expanded the aggregate 3% rule for audit committee elections, renamed outside directors as “independent directors,” and mandated hybrid AGMs from January 1, 2027. The FSCMA enforcement decree, effective December 31, 2024 — prohibited treasury stock allocation in mergers and spinoffs, closing the most abused governance loophole in modern Korean capital markets.

The Corporate Value Up program, launched February 2024, has now crossed 590 disclosure filings. KRX announced on April 15, 2026 that the simplified disclosure path will be eliminated in 2027 — full plans with status diagnosis, target setting, implementation timeline, and communication strategy will be required. KRX will publish a “low-PBR list” in H2 2026 designed to name and shame companies that have not engaged.

Korean activists now hold real war chests. Align Partners runs ₩1.235 trillion in AUM and has filed AGM proposals at six small-caps in the last 12 months. Dalton Investments has accumulated 5%+ stakes across multiple cosmetics, holdco, and mature-industrial names. Truston has campaigned at BYC since 2021. KCGI executed the first ownership change at Hanyang Securities in 68 years.

These are not promises. They are enacted laws, court precedents, and active capital deployments. The Korea Discount existed because the legal architecture justified it. The legal architecture is now changing faster than institutional pricing has adjusted.

That gap is the trade.

What I’m doing with personal capital

I’m currently building a 15-name basket of Korean equities across three theses: AI infrastructure suppliers selling into the NVIDIA, Micron, SK Hynix, Samsung and TSMC supply chains; deep-value small caps trading below tangible book with named institutional activists on the register; and founder-succession setups where inheritance tax of 50-60% on controlling shares structurally forces value-realizing events.

I’ll be deploying capital into these positions over the coming weeks, building the most liquid names first and accumulating the smaller positions over 4-8 weeks. This is personal capital with a 5-10 year horizon, not a short term trade. Position sizes and entry timing will be a function of liquidity constraints, not narrative urgency.

I’ll be transparent about which names I purchase and at what levels. Not all 15 will be sized equally. Some I’ll own forever. Some I’ll own for 24 months around a specific catalyst. The basket is calibrated to a regime change, not a single thesis.