The Ice Is Cracking

A consumer credit crisis hiding in plain sight

How a forensic deep-dive into Sallie Mae’s (SLM) filings revealed $2.1 billion in phantom earnings, a consumer credit crisis hiding in plain sight, and the widest disconnect between reported metrics and reality I’ve ever seen.

The Canary Just Died

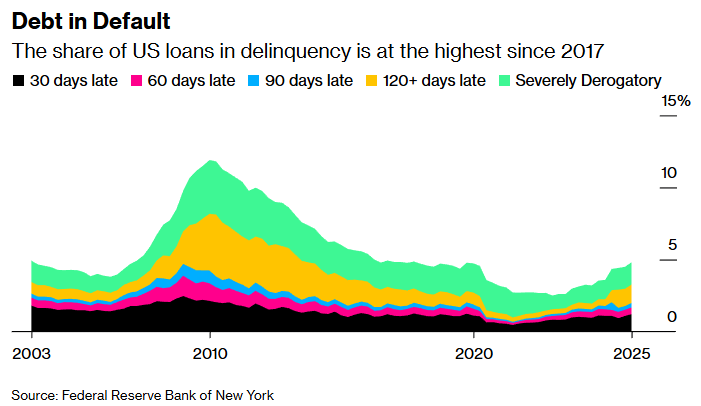

This week, the New York Fed released its latest consumer credit data. The numbers are ugly. US loan delinquencies just hit their highest level since 2017, with every category — auto, credit card, mortgage — trending worse.

But one category isn’t just trending worse. It’s in freefall.

Student loans.

The aggregate picture is bad enough → delinquencies across all consumer debt categories are rising simultaneously. But zoom into the loan-type breakdown and the story gets much worse.

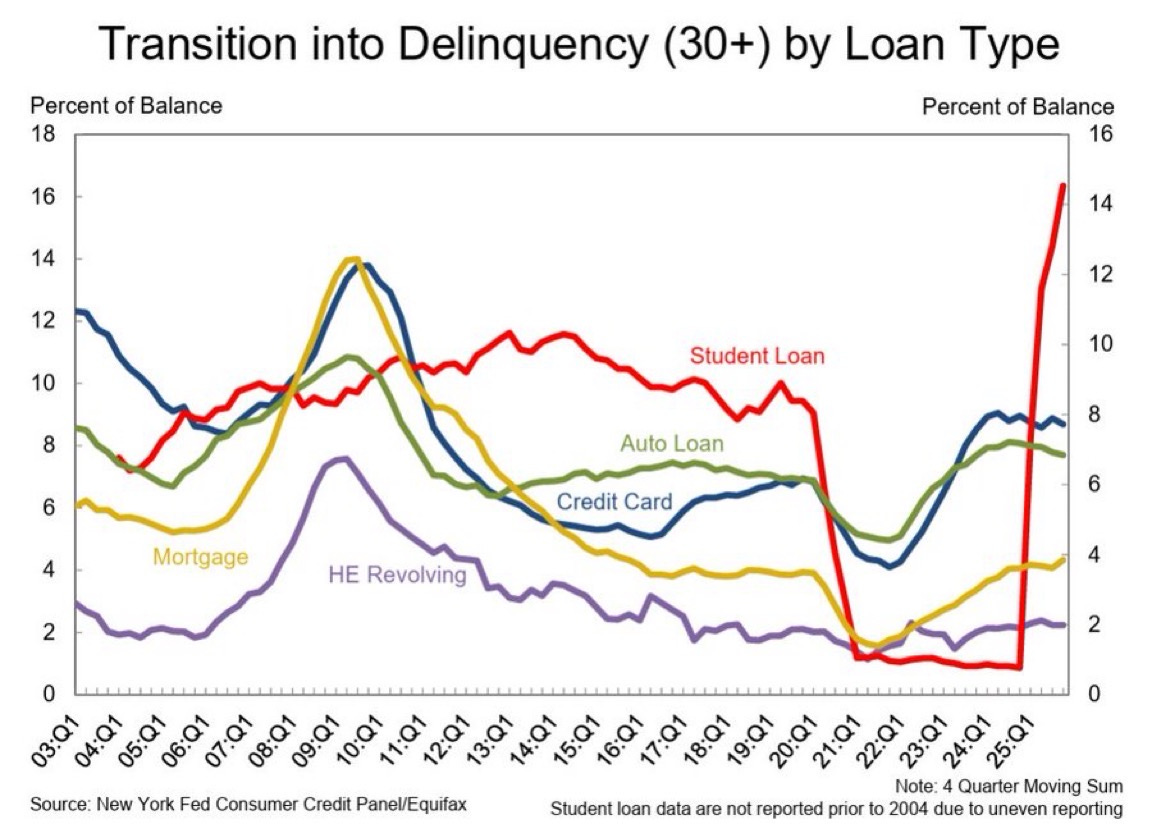

The transition rate into 30+ day delinquency for student loans just hit 16% — the highest on record since the Fed started tracking in 2004. That red line going vertical isn’t a blip. It’s a structural break.

Now look at who’s breaking:

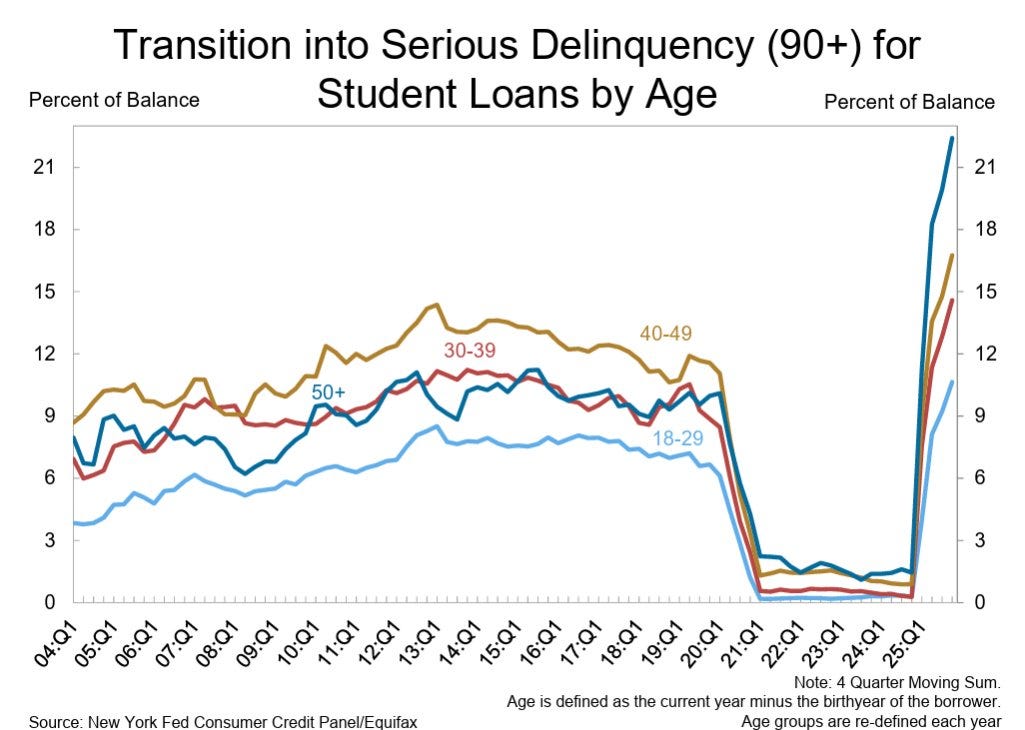

For borrowers aged 18-29, the 90+ day serious delinquency rate spiked to ~10%. But this isn’t just young borrowers — every age cohort from 30-39 to 50+ is showing sharp vertical moves to 21%+. When all demographics break simultaneously, you’re looking at a systemic problem, not an isolated pocket of stress.

Let that sink in. More than one in ten young borrowers with student debt are now seriously delinquent. This isn’t a crack in the foundation. It’s a structural failure.

And there’s one company sitting right on top of the fault line: SLM Corporation — Sallie Mae.

What the Market Sees

On paper, SLM looks like a well-run consumer finance company. Market cap of $5.4 billion. Trading at 2.0x tangible book value. P/E around 9x reported earnings. Aggressive buybacks — 16% of shares retired over 3 years. CET1 capital ratio at 11.3%. Delinquencies “improving” — 3.68% vs 3.90% prior year.

The stock is up 342% over 5 years. Wall Street sees a high-ROE compounder returning capital to shareholders. The consensus sell-side view is “stable credit, strong capital return, buy the dip.”

They’re reading the wrong page!!

What the Filings Actually Say

I pulled SLM’s 10-K and ran it through the same forensic methodology I use for every position. Balance sheet archaeology. Cash flow forensics. Footnote mining. Incentive structure analysis.

What I found is a company where GAAP earnings and economic reality have completely diverged.