The Doomers Got It Wrong: AI Is Building a Bigger Pie, Not Stealing Your Slice

AI won't take your job. Learn how to use AI, or be left behind.

The consensus narrative for the past two years has been relentless: AI is coming for your job. Every quarter, every earnings call, every think-tank white paper seemed to inch closer to the same dystopian conclusion — a wave of automated displacement, hollowed-out white-collar employment, and a labor market that simply wouldn’t recover.

I’ve been skeptical of that framing for a while. And this week, Citadel Securities published a piece that puts the institutional weight of one of the most rigorous macro research shops on Wall Street squarely behind the contrarian view.

The title: The Economics of Intelligence.

The conclusion: AI is a complement to labor, not a substitute — and the data are already proving it.

What Citadel Actually Found

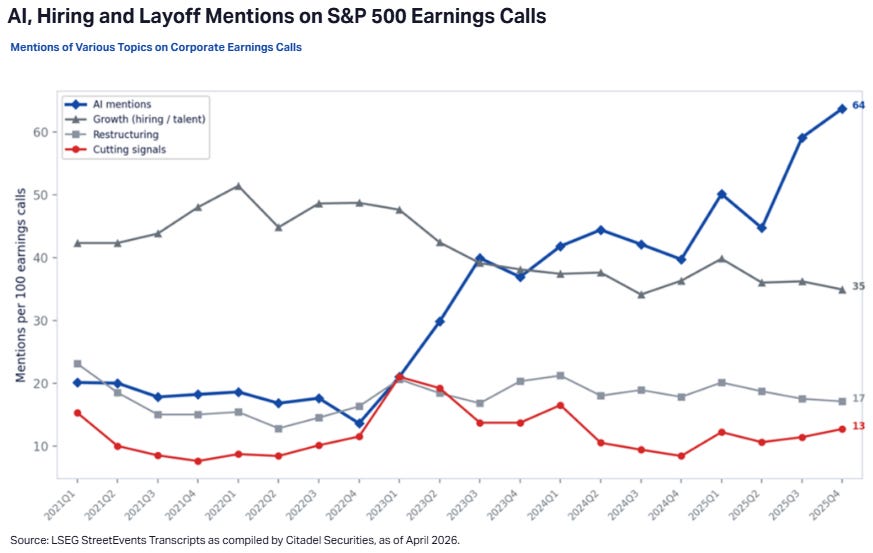

Frank Flight and the Citadel Securities macro team did something most AI commentators haven’t bothered to do: they looked at the actual data.

Their analysis ran NLP-based keyword classification across S&P 500 earnings call transcripts, tracking how corporate executives have framed the relationship between AI and their workforces over time. The results are striking.

AI mentions on S&P 500 earnings calls grew from 20% to 64% of companies — a near-tripling that began accelerating sharply after ChatGPT launched in early 2023. If AI were actually gutting headcount, you’d expect that acceleration in AI adoption to correlate with aggressive labor cutting signals.

It doesn’t.

Labor cutting language — layoffs, severance, hiring freezes — peaked at 21% in Q1 2023 and subsided to 13% by Q4 2025. Hiring and talent language has remained steady. Restructuring language hasn’t budged. The AI adoption wave, in the actual corporate data, has not produced a labor market shock.

But here’s the number that stops me cold:

When executives mention AI alongside their workforce, they frame it as a complement to labor vs. a substitute by a ratio of roughly 8 to 1. 43% of firms call AI a complement. 51% are neutral. Only 5 → five percent, frame AI as a substitute for human labor.

These are not Silicon Valley futurists or ideologically motivated academics. These are CEOs and CFOs on earnings calls, speaking to institutional investors, where credibility is literally priced in. They are telling you, under that scrutiny, that they are using AI to make their existing people more productive — not to replace them.

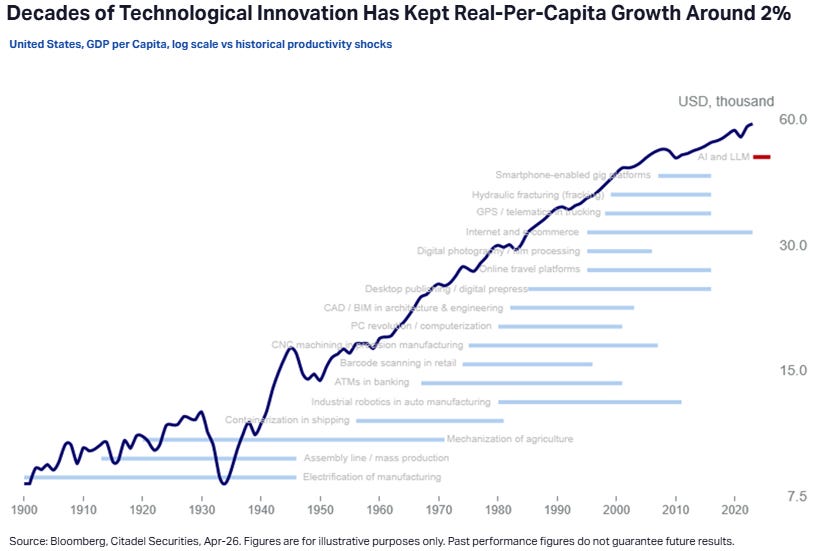

The Physics Argument: Why Compute Intensity Changes Everything

Citadel’s framework builds on a structural argument that I find compelling from first principles, and one that maps directly onto my own research from earlier this year on AI infrastructure constraints.

The core thesis has four linked components:

1. Compute demands scale quadratically with task complexity. This is not intuitive, but it’s crucial. The jump from automating a simple task — summarizing an email, generating a code snippet — to automating a complex, multi-step cognitive role is not linear. It requires orders of magnitude more compute. The physical constraints are real: silicon, power, cooling, data center buildout. These don’t scale overnight.

2. Physical scarcity limits generalized displacement. Because complex cognitive work is expensive to automate at scale, the economics favor augmentation over wholesale replacement. It is cheaper and faster to give a skilled worker an AI co-pilot than to build and run the compute stack that could fully replace them.

3. AI therefore integrates into existing workflows as a force multiplier. This is the radiologist story. This is the lawyer who drafts in half the time. This is the analyst who can synthesize ten earnings calls before the market opens. The tool makes the human more productive without eliminating the human’s indispensable judgment, relationships, and accountability.

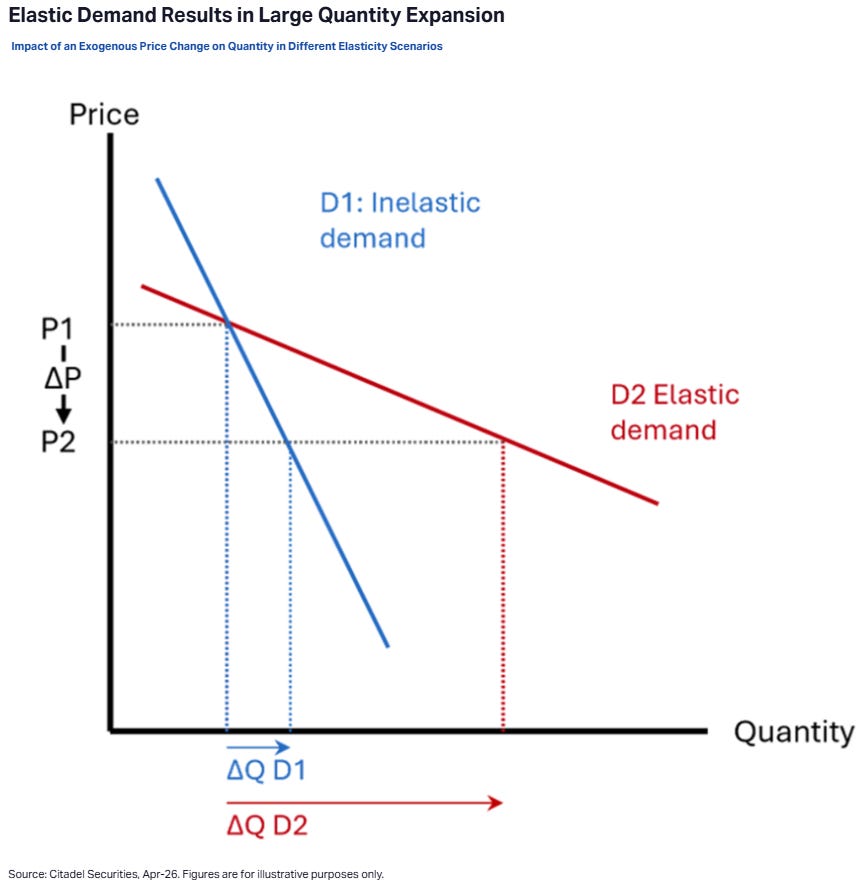

4. History says this is the pattern — and demand is elastic. Technological revolutions don’t eliminate labor as an input. They alter the task composition of jobs while output expands to fill the new productive capacity. Microsoft Office didn’t replace office workers. It redefined what office workers could do — and the economy created more of them.

As Citadel puts it directly: “Was the advent of Microsoft Office a complement or substitute for office workers? Ex-ante the concern skewed towards substitution, ex-post it appears a clear complement.”

That’s the bet we’re making again, and the early data are on the right side of it.

Jevons Paradox: The Demand Expansion Nobody Is Modeling

There’s a concept embedded in Citadel’s analysis that I think is the most underappreciated macro dynamic in the AI debate: Jevons Paradox.

Named after 19th century economist William Stanley Jevons, who observed that more efficient coal-burning engines actually increased total coal consumption — because efficiency drove adoption and expanded use — the paradox describes how productivity improvements in a resource often increase total demand for that resource rather than reducing it.

Applied to AI and labor: as AI makes workers faster and more productive, the economy doesn’t simply need fewer workers. It expands the scope of what gets done. More tests get run. More clients get served. More software gets built. The demand for skilled human judgment scales with the expansion of output, not against it.

We’re already seeing this in the construction labor market. AI data center buildout is driving a measurable pickup in construction hiring. The infrastructure layer of the AI revolution is physically employing people. This is Jevons working in real time.

Jensen Has Been Saying This for Months — And He Was Right

I want to give credit where it’s due. Jensen Huang has been in front of this thesis longer than anyone in the financial media has taken seriously.

His radiologist example has become something of a signature argument, and for good reason — it is devastating to the displacement narrative.

Ten years ago, Geoffrey Hinton — the so-called “Godfather of AI” — predicted that AI would make radiologists obsolete. His technical forecast was correct: AI is now embedded in nearly every corner of radiology. But the labor outcome was exactly the opposite of what he predicted.

As Huang explained at the Milken Institute this week: “People who believe this misunderstand that the purpose of a job and the task of a job are related but not ultimately the same thing.”

The radiologist’s job is to diagnose disease. Reading scans is a task in service of that purpose. When AI made image analysis faster and more precise, radiologists could read more scans, serve more patients, and generate better economics for hospitals. The response? Hospitals hired more radiologists. The American College of Radiology projects the number of radiologists in America will grow by up to 40% between 2023 and 2055.

Huang has extended this logic broadly. In his recent appearance at the Milken Institute: “AI creates jobs. AI is the United States’ best opportunity to re-industrialize itself.”

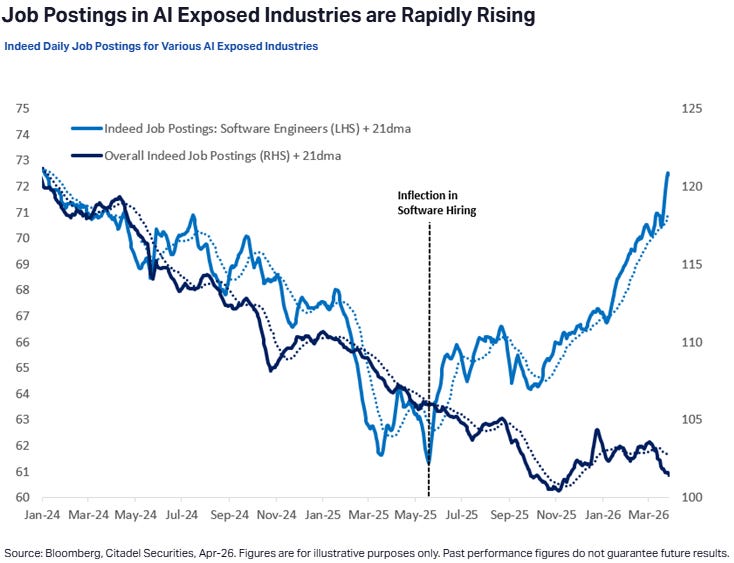

And the data is starting to confirm it. Software engineer job postings on Indeed were up 11% year-over-year in early 2026 — in the middle of what was supposed to be an AI-driven tech layoff wave. Huang himself noted that AI has created more than half a million jobs in recent years.

“I’m fairly confident that AI will drive productivity, revenue growth, and therefore more hiring,” he said.

The inflection is happening. We’re watching it in real time.

The Macro Positioning Read

For those of us managing capital, what does this framework actually imply?

Citadel’s analysis makes an argument that I think has real alpha embedded in it: the market has been pricing AI as a labor destroyer, and that consensus is wrong. Sectors like Software IGV 0.00%↑ have been brutally sold-off the past year; which if you believe in this color — then software presents an amazing opportunity. As evidence accumulates that AI adoption is not producing the employment shock the doomers forecast, several second-order effects follow:

Wage growth remains stickier than feared → inflationary impulse doesn’t disappear the way bears assumed

Consumer spending holds up better than recession models embedded in AI-displacement scenarios → consumer staples and discretionary don’t get the demand shock

AI infrastructure investment remains front-loaded and massive → the real challenge is the payoff structure (decades of productivity gains vs. near-term capex) not the demand destruction narrative

The big winner remains the infrastructure layer: compute, power, data centers — the physical real estate of intelligence

The Citadel piece explicitly flags what I think is the real risk to the AI trade: not that AI destroys jobs, but that the investment cycle is heavily front-loaded while the productivity payoff accrues over decades. That’s a very different bear case than the labor displacement narrative — and it’s a bull case for the physical infrastructure names I’ve been long. ETN 0.00%↑& GEV 0.00%↑.

The pie is getting bigger. The question for investors is simply: who has the biggest fork?

Disclaimer: This is for Educational Purposes Only. NFA.