The Crowded Short: Why Every Investor is Betting Against Inflation's Return

A Quantitative Analysis of Market Complacency and Tail Risk Exposure

Citadel Securities’ Nohshad Shah just dropped one of the most important macro notes of Q1 2026, and the institutional implications are massive. The core thesis? Markets, governments, central banks, equities, and fixed income are all structurally levered to the productivity story → making everyone effectively short the inflation tail.

Let me break down why this matters for systematic traders and where the asymmetric opportunities lie.

The Productivity Mispricing: A J-Curve Reality Check

Shah’s analysis exposes a critical disconnect in how markets are pricing AI-driven productivity gains. The 5y5y forward inflation break-evens have completely decoupled from the cyclical outlook. Essentially, markets are betting that the economy can run hot without generating inflation because AI productivity gains will expand supply-side capacity fast enough to absorb demand.

The problem? History shows technological productivity gains follow a J-curve trajectory. The impact is incremental and compounds over years, not immediate. Markets are front-running productivity improvements that may take 3-5 years to materialize while simultaneously expecting steep disinflation in H2 2026 alongside strong cyclical acceleration.

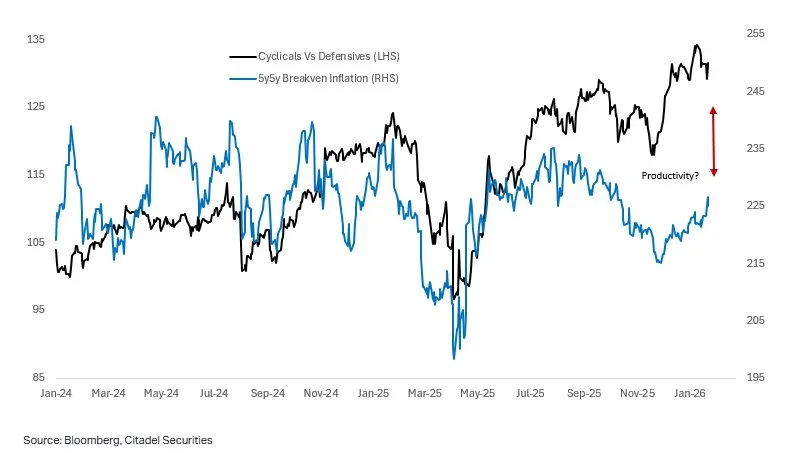

The Key Chart: Cyclical Stocks vs 5y5y Inflation Expectations

Shah’s chart showing the disconnect between cyclical stock performance and 5y5y inflation breakevens is critical. Historically, when cyclical stocks rip, inflation expectations rise in tandem. Today? Cyclicals are surging while inflation expectations remain anchored—the market is pricing in simultaneous strong growth AND disinflation, predicated entirely on productivity gains that are extremely difficult to measure in real-time.

The LRMI take: Productivity is calculated as a residual and only observable through macroeconomic outcomes. By the time markets realize they’ve over-indexed to short-term AI productivity, inflation will already be realizing higher than expected. This is a classic information lag problem that creates exploitable convexity.

The Fiscal Profligacy Problem: Global Debt Dynamics

Japan’s Warning Shot

The BOJ’s emergency intervention this week after PM Takaichi proposed a ¥0.7% GDP consumption tax cut (on top of 3% GDP fiscal expansion) demonstrates how fragile global bond markets have become. When buyers’ strikes hit major fixed income markets, central banks must choose between:

Market functioning (emergency purchases → financial repression)

Currency stability (letting yields clear → FX depreciation)

Inflation credibility (restrictive policy → economic pain)

There’s no free lunch. Japan chose option 1, which means ongoing pressure on JPY and inflation expectations.

The US Exceptionalism Premium

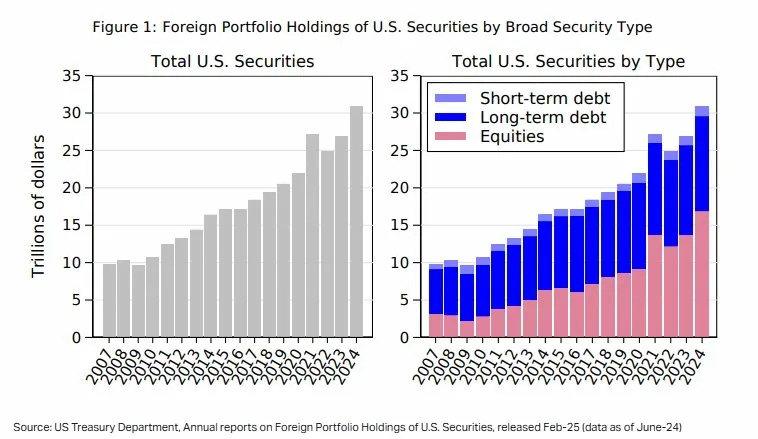

Foreign investors own 33% of outstanding Treasuries, 27% of corporate debt, and 18% of equities—totaling $30.9tn in US securities. The dollar’s reserve currency status creates structural demand, keeping term premia artificially compressed relative to fundamentals.

But here’s the critical insight: US debt is still growing faster than GDP, which definitionally puts debt/GDP on an unsustainable trajectory. The market is betting AI productivity solves this before it becomes problematic. Shah notes that while there’s no imminent catalyst, the ramifications of sustained loss of confidence in US fiscal position would be “significantly more global in nature and severe in impact” than UK or Japan episodes.

The Geopolitical Volatility Regime: Power Over Rules

The Greenland episode crystallized the new paradigm: we’re in a geopolitical order driven by power rather than rules. When Trump’s Greenland acquisition bid hit, markets reacted immediately:

NDX: -2%

DXY: -1%

30Y UST yields: +12bps

Even though these moves partially reversed, the volatility spike demonstrates that policy-driven exogenous shocks are now a feature, not a bug. As Canada’s PM Mark Carney argued at Davos, the rules-based international order is dead—great-power rivalry is the new framework.

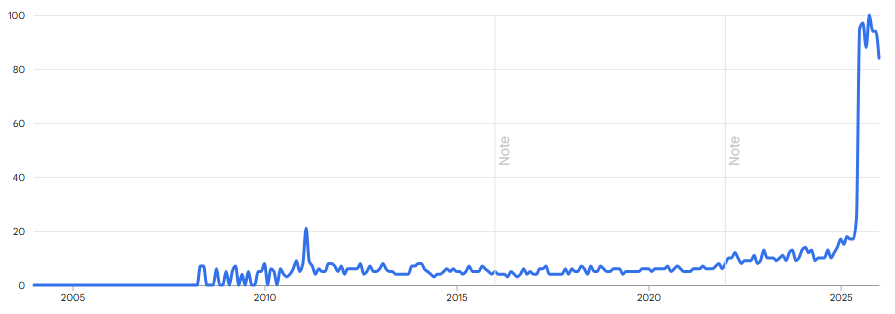

The Arctic Security Search Volume Chart

Shah included a brilliant visualization: Google search intensity for “Arctic security” was essentially zero until January 2026, then spiked vertically. This is how quickly the Overton window shifts in the current regime. Short-vol, carry-based strategies are structurally mispriced for this environment.

LRMI Systematic Framework: Identifying the Trade

The Setup

This is textbook:

Asymmetric payoff structure: Limited downside on inflation hedges vs exponential upside if productivity story disappoints

Consensus positioning: Everyone is structurally short inflation tail → liquidity vacuum in tail scenarios

Multiple catalysts: Fiscal dominance, energy constraints, sticky labor markets, geopolitical disruption

Volatility mispricing: Implied vol on commodity complex at 3-year lows despite structural risks

Market Positioning Evidence

TIPS Break-evens: Compressed despite M2 velocity inflection

VIX Term Structure: Persistent backwardation = macro hedge unwind

Commodity Vol Surface: 6+ month implied volatility at multi-year lows

Inflation Swaps: Net short positioning at levels not seen since Q4 2020

Expression Strategy

Core Position (2-5% portfolio allocation, 12-18 month horizon):

Long-dated OTM calls on commodity volatility (particularly energy and grains)

Inflation-linked sovereign exposure with positive carry characteristics

Tactical precious metals beta (GLD/SLV positioning into supply constraint scenarios)

Short duration positioning in rates (via TBT or outright Treasury shorts)

Risk Management

This is a convexity trade, not a directional bet. Patient capital and disciplined sizing are essential. The productivity story could still play out over 2-3 years, meaning we could see continued disinflation in the near term before the regime shift materializes.

Key monitoring metrics:

Core PCE vs market expectations divergence

Real wage growth acceleration

Commodity supply/demand balances

TIPS break-even spread compression/expansion

VIX term structure slope changes

The Bottom Line

Shah’s note crystallizes what LRMI’s quantitative models have been signaling: markets are positioned for a best-case scenario that requires flawless execution on multiple fronts simultaneously. The goldilocks narrative of easy financial conditions, strong growth, AND disinflation requires:

AI productivity gains materializing immediately (not historically realistic)

Fiscal trajectories stabilizing (not happening globally)

Geopolitical stability (clearly deteriorating)

No commodity supply shocks (Middle East/Black Sea risks elevated)

When one assumption fails, the cascading effects will be non-linear because everyone is on the same side of the boat.

The systematic opportunity isn’t predicting which catalyst triggers first—it’s positioning for the inevitable volatility expansion when consensus realizes they’ve mispriced the tail. That’s what the inflation convexity trade offers: cheap optionality on a regime shift that fundamentals suggest is higher probability than markets currently discount.

Read the full Citadel Securities analysis here

Risk Disclosure: This analysis is for informational purposes only and does not constitute investment advice. Tail risk positioning requires patient capital and sophisticated risk management.