SK Hynix just dropped one of the greatest earnings reports in semiconductor history.

Memory just became an AI infrastructure monopoly. The market still hasn't fully noticed.

SK Hynix just posted a 72% operating margin in a seasonally weak quarter. Revenue tripled year-over-year. The CFO said customer demand exceeds supply for the next three years. The stock is still priced like a cyclical. That's the trade.

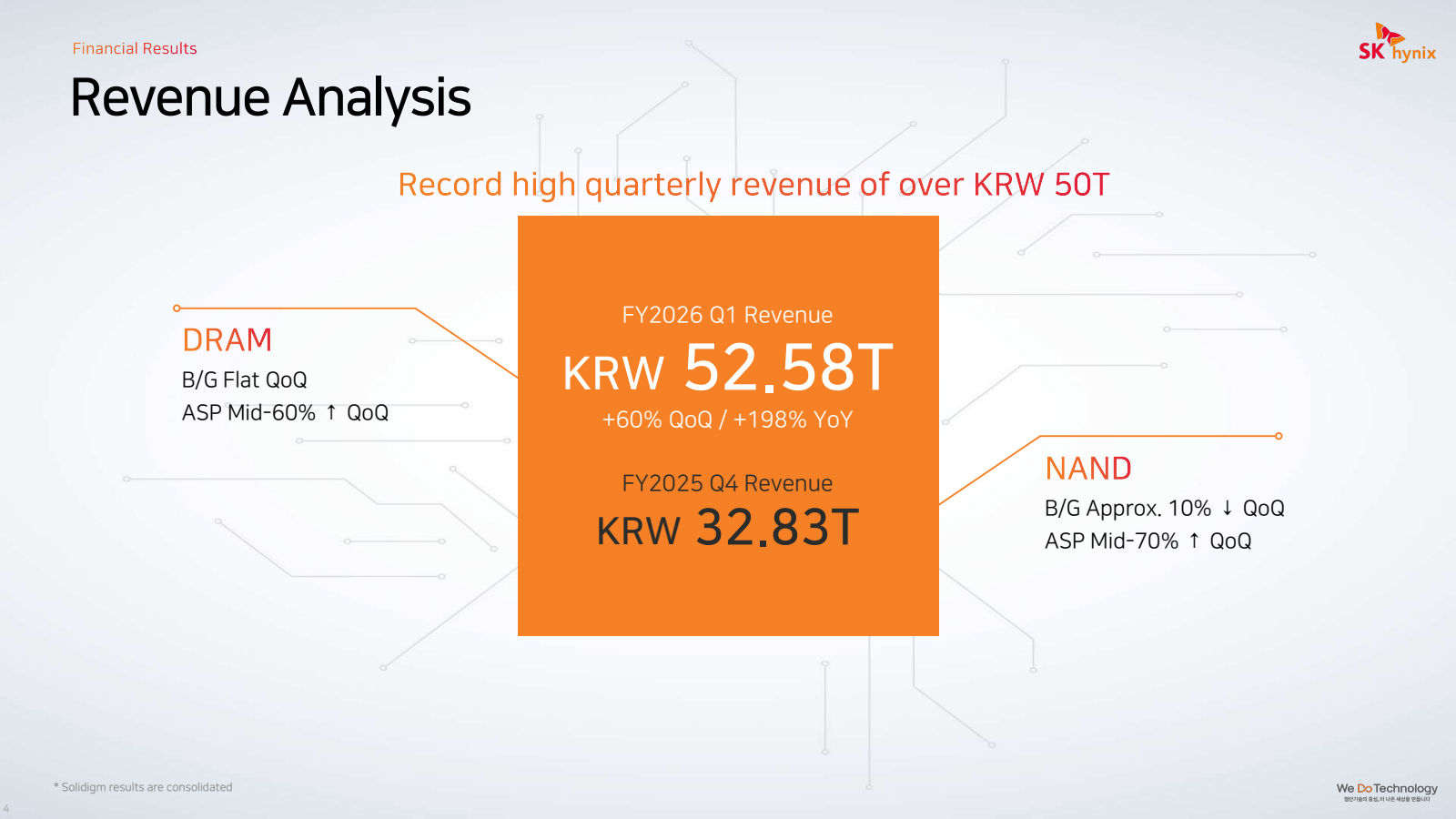

Revenue: ₩52.6T +198% YoY · beat est +7%

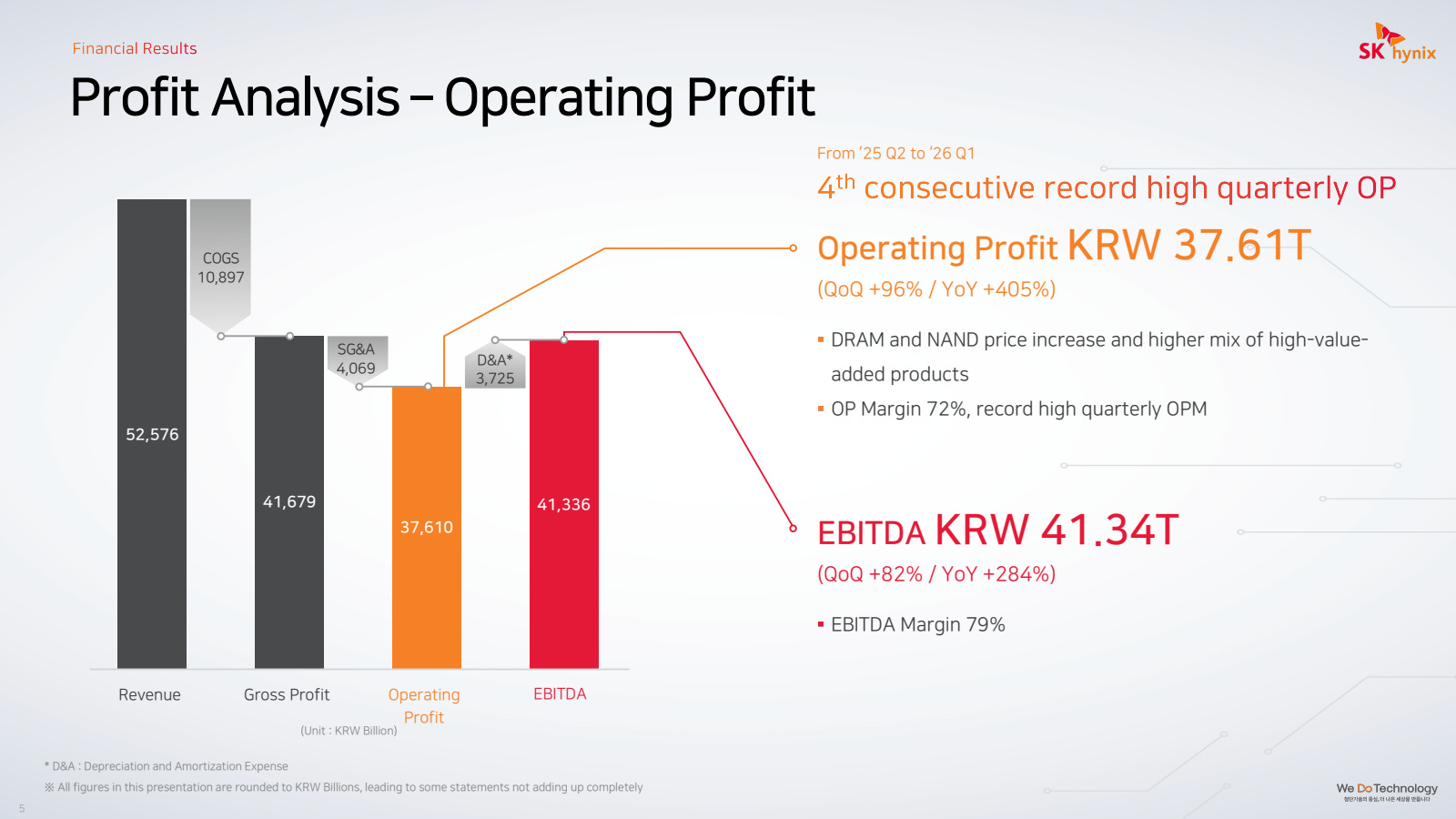

Op. Margin: 72% record · +30pp YoY

EBITDA: ₩41.3T 79% margin · beat est

Net Cash: ₩35T flipped from net debt

This quarter was not supposed to be possible

To put 72% operating margins in context: Apple, the most profitable consumer hardware company in history, runs at roughly 30%. SK Hynix — a Korean memory manufacturer that analysts have modeled as a commodity cyclical for two decades — just more than doubled that, in Q1, which is historically their softest seasonal quarter.

Revenue hit ₩52.58T, up 60% from the prior quarter and 198% year-over-year. DRAM average selling price surged mid-60% quarter-on-quarter with flat bit growth — meaning the entire revenue jump was pure pricing power, not volume. NAND ASPs were up mid-70% QoQ. This is not a demand-pull inventory cycle. This is structural scarcity pricing.

Four consecutive record operating profit quarters — Q2 '25 through Q1 '26 — with COGS rising only 6% QoQ on 60% revenue growth. That is what operating leverage looks like when a commodity business stops being a commodity.

“Customers’ demand for the next 3 years far exceeds our current supply capacity. Within the limited supply capacity, we are doing our best to supply as much HBM as possible to our customers.”

— Kim Gi-Tae, Head of HBM Sales · SK Hynix Q1 2026 Earnings Call

A three-year demand visibility statement. In memory semiconductors. That has never happened before in this industry's history.

LRMI Derivative Analysis: Where we are in the cycle: momentum, acceleration, jerk

Most earnings recaps will tell you revenue went up. Here's the more interesting question, I’ve developed: is the rate of improvement getting faster or slower? Running the three mathematical derivatives on quarterly revenue gives a precise cycle positioning signal most analysts never compute.