Operation Ghost Charter

The Market Is Pricing Fannie and Freddie Like They'll Never Leave Conservatorship. That Window Is Closing.

Last night, Bill Ackman — who holds roughly 10% of Fannie Mae and Freddie Mac’s public float through Pershing Square — posted nine words that set financial Twitter on fire:

“And Fannie and Freddie are stupidly cheap. Asymmetry at its best. They could be a 10X and it could happen soon.”

2.6 million views in under 24 hours. Then Michael Burry — the “Big Short” guy, @michaeljburry — replied with: “Cannot emphasize enough how rare this is in this market.”

Two of the most credentialed contrarian investors alive, publicly aligning on the same trade, at the same moment. I’ve been building this thesis for months. This is the writeup I’ve been working toward.

What Fannie Mae and Freddie Mac Actually Are

If you haven’t thought about these companies since 2008, here’s the 60-second version.

Fannie Mae (FNMA) and Freddie Mac (FMCC) are the two government-sponsored enterprises — GSEs — that underpin approximately 70% of the U.S. mortgage market. They don’t originate mortgages. They buy them, package them into mortgage-backed securities, and guarantee them. They are the plumbing of American homeownership.

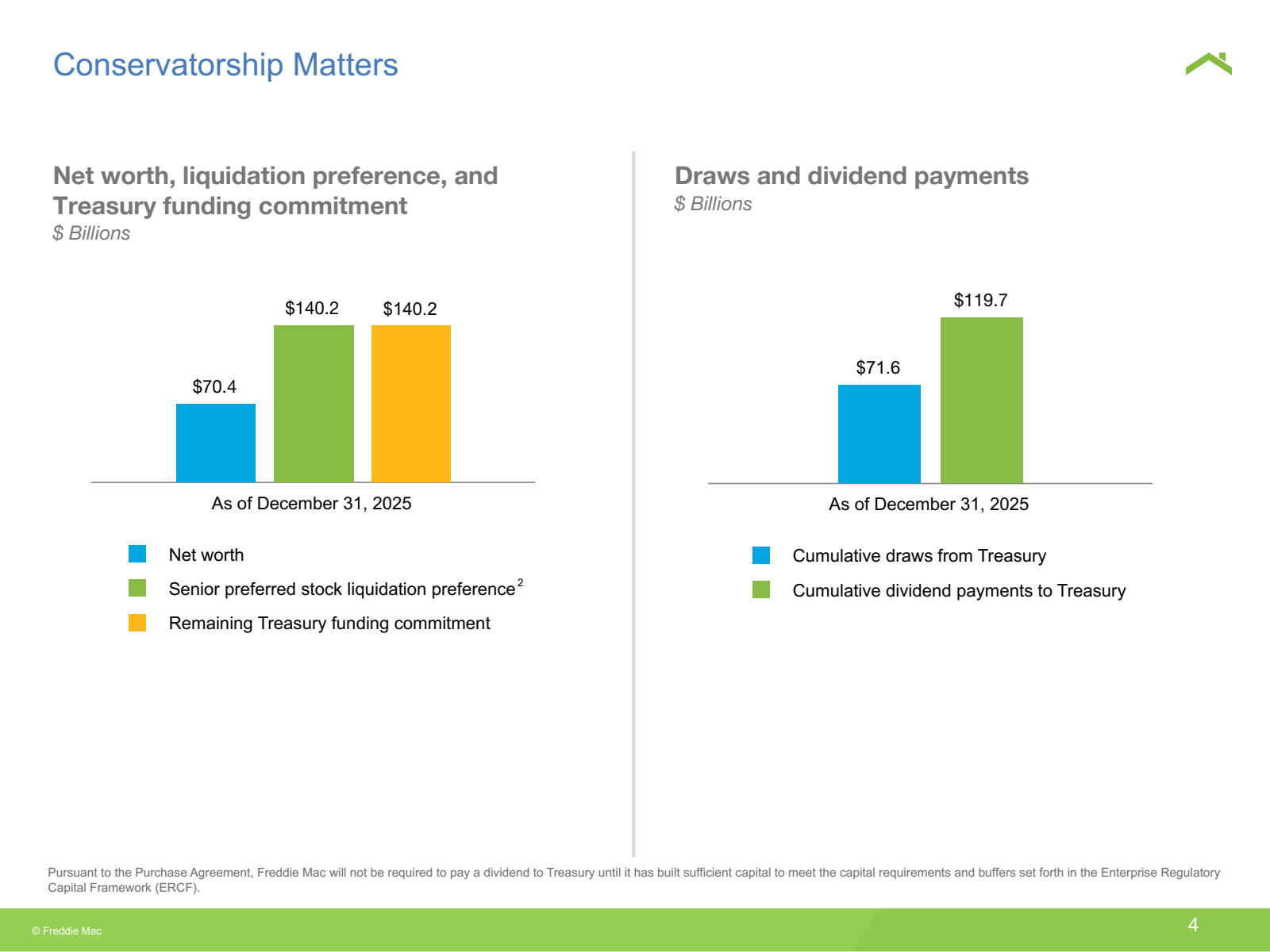

In 2008, they nearly collapsed under the weight of subprime exposure. The government took them into conservatorship under the FHFA, injected $193 billion, and has controlled them ever since. The original deal: all profits get swept to Treasury. That “net worth sweep” continued for years — by the time it was amended in 2021, Fannie and Freddie had already returned over $300 billion to the U.S. government. They repaid the bailout in full, with a substantial premium on top.

Since 2021, they’ve been allowed to retain earnings. And the capital accumulation that followed is the most important number in this thesis.

The Second Derivative Nobody Is Watching

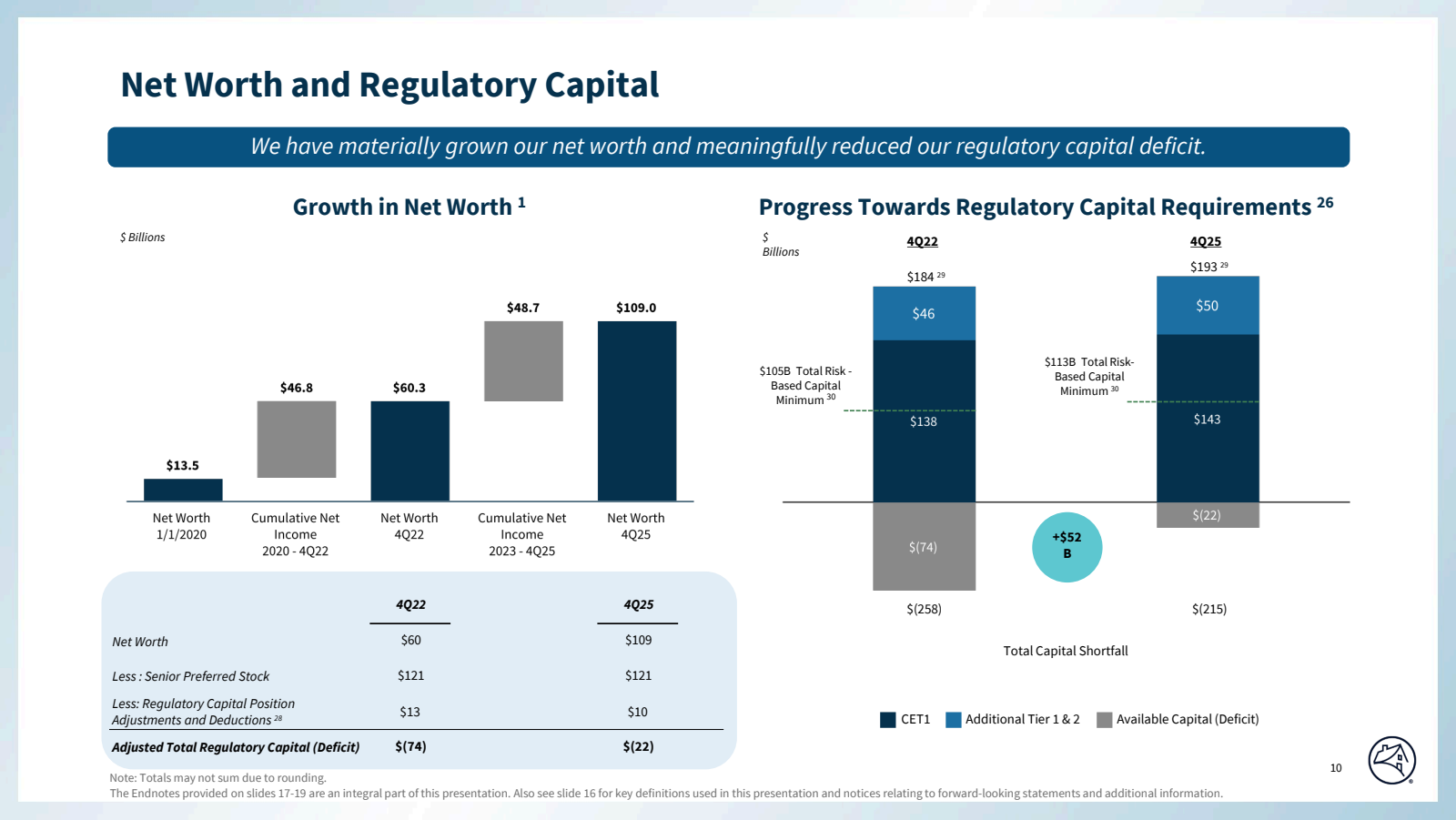

Fannie Mae’s total equity: $47 million in FY2021. $109 billion by FY2025. That is $95.5 billion of capital accumulation in five years — not from government transfers, but from retained earnings on a $14+ billion annual earnings machine.

Freddie Mac went from $28 billion in equity to $70.4 billion over the same period.

The rate of accumulation matters more than the level. These entities are compounding equity at scale, every quarter, like a clock. Meanwhile, operating costs are falling — Fannie cut noninterest expense by $141 million year-over-year in 2025, including a $40 million reduction in administrative expenses from headcount cuts and contract renegotiations. Freddie’s noninterest expenses fell to $8.6 billion, down $38 million year-over-year.

Revenue up. Costs down. Equity compounding. In any normal corporate context, this trajectory commands a premium multiple. These stocks trade at roughly 0.1x book value on Fannie and 0.04x on Freddie.

Why? Because they’re still in conservatorship — and most institutional investors literally cannot own them.

The Perception Gap: Why Nobody Owns This Yet

This is the core of the asymmetry. Run through who can’t own FNMA/FMCC right now:

Dividend and income funds — no dividends under conservatorship. Hard screen out.

ESG mandates — government-controlled, governance red flags. Hard screen out.

Active growth managers — no CEO, no strategic autonomy, FHFA controls everything. Pass.

Style-box investors — not classified as a bank, insurer, or fintech. Doesn’t fit the box.

Index funds and quants — OTC-traded, not listed on NYSE or Nasdaq. Not in the index.

Risk-managed macro funds — political binary risk. Avoid.

Every single one of these constraints evaporates upon conservatorship exit. A re-listing, a PSPA restructuring, or a permanent CEO appointment would force a mass reclassification of these securities across hundreds of institutional mandates. That forced reclassification is the re-rating mechanism. The buyer base that doesn’t exist today would materialize overnight.

The Capital Shortfall: What It Is and Why It Matters

Freddie Mac stated explicitly on their Q4 2025 earnings call: “Capital shortfall to regulatory capital, excluding buffers, was $106 billion because the $73 billion of senior preferred stock does not qualify as regulatory capital.”

That sentence is doing a lot of work. The shortfall is not an operating insolvency. It’s a structural accounting artifact. The senior preferred stock owed to Treasury doesn’t qualify as regulatory capital under the ERCF framework — so on paper, the capital gap looks enormous. In reality, any PSPA restructuring that converts, cancels, or reclassifies that Treasury preferred could eliminate the shortfall essentially overnight.

Management didn’t bury this disclosure. They surfaced it, explained the mechanism, and named the instrument. That’s not an accident — that’s an invitation for sophisticated investors to model what the re-rating looks like if the preferred gets restructured.

Ackman has done exactly that. His base-case valuation, using 16x and 13x estimated 2026 earnings respectively, gets you to approximately $34/share for both entities at IPO. From FNMA’s current price around $4.86 and FMCC around $4.38, that’s roughly 600–700% upside in his base case. If they revisit pre-2008 levels in the mid-$40 range, you’re looking at roughly 900% upside from current prices. Stocktwits

What Burry Actually Said — And Why It’s More Important Than Ackman’s Tweet

Burry’s amplification was notable — but his full framing is more nuanced than the retweet suggests. According to Seeking Alpha, Burry now sees FNMA and FMCC IPOs as a 2027 proposition at best. Seeking Alpha He’s not calling for a near-term catalyst. He’s calling for the trade to be real, the thesis to be valid, and the timeline to extend — which means the entry window is still open.

This is actually the most constructive possible framing for a new position. The “stupidly cheap” language with a 2027 timeline is Burry saying: the market has overcorrected on timeline pessimism. Both stocks have lost more than half their value over the past six months, reaching their lowest levels in a year GuruFocus — not because the earnings thesis broke, not because privatization became less likely structurally, but because a Bloomberg article reported that a planned 5% secondary offering stalled.

The reaction to that stall is the mispricing. A failed secondary offering isn’t a failed privatization thesis — it’s a scheduling delay.

The Management Signal You’re Not Supposed to Notice

Management of both GSEs cannot speak openly about conservatorship exit. They are regulated entities under FHFA control. But they can change who they’re speaking to and how.

On Freddie Mac’s Q1 2025 earnings call, CFO Jim Whitlinger named FHFA Director Bill Pulte by name — explicitly, on a public earnings call — and connected regulatory reform directly to revenue growth and net worth accretion. He called it a roadmap for a better U.S. housing finance system. Compare that to Q4 2024, where the same CFO spoke exclusively about financial metrics with zero mention of the transformation agenda.

Three calls in, the messaging cadence is different. That’s not boilerplate drift. That’s positioning language for an investor base that doesn’t exist yet.

At Fannie Mae, a new Acting CEO — Peter Akwaboah — opened his first full-year earnings call by describing his tenure as happening “at such a pivotal time.” New leadership, mid-conservatorship, front-loading a phrase like “pivotal time” in his opening remarks. That’s not coincidental language.

The conspicuous absence of the words “privatization,” “IPO,” or “conservatorship exit” in either company’s transcripts is the tell. They are prohibited from front-running policy. The playbook is silence + capital build + efficiency narrative. They’re executing it precisely.

The Bear Case (I’m Not Ignoring It)

The single biggest structural risk is Treasury warrant dilution. The federal government holds warrants to acquire 79.9% of common equity in both entities. Even in a favorable privatization scenario, existing common shareholders could face severe dilution depending on how those warrants are exercised. If the warrant structure isn’t restructured in a shareholder-friendly way — and there’s no guarantee it will be — the common equity upside gets capped or eliminated entirely. This is the variable that determines whether this is a double or a washout.

The second risk is political binary. This trade lives and dies on one administration’s political calendar. A policy reversal, a housing market shock, Congressional pushback from Elizabeth Warren’s coalition — any of these can stall the thesis indefinitely. Sen. Warren has stated publicly she is “very worried that the Trump administration is very focused on how the billionaires are gonna do in any Fannie/Freddie deal.” NPR That’s a real political headwind.

Third: investor confidence in the Trump administration’s plan to sell additional shares of Fannie Mae and Freddie Mac is waning, as the initiative has stalled with no significant updates. GuruFocus Timeline risk is real. The 2026 IPO window that Ackman projected is closing.

The fourth risk is earnings deceleration — Fannie’s net income has fallen from $22.2 billion in FY2021 to $14.4 billion in FY2025. Freddie has been range-bound at $10-12 billion for three years. Credit normalization and rising multifamily delinquencies are real headwinds that could slow the capital build.

How to Size This

This is not a core position. This is a 3–5% starter to core, time-gated thesis with an embedded binary option.

The asymmetry math is straightforward: at Ackman’s base case, this is a 6–7x from current prices for the common in a favorable scenario. At his earnings multiple range with a NYSE re-listing, you get meaningful institutional forced-buying on top of the fundamental re-rating. The upside is real and math-able.

The downside is also real — common equity in a conservatorship has no fundamental floor. If the warrant structure doesn’t resolve favorably, existing common shareholders could see near-zero outcomes even in a technically “successful” privatization.

Watch the VIX and credit spread environment as your regime filter. This thesis works better in a risk-on backdrop with tightening credit spreads. In a risk-off credit event while both entities are still in conservatorship, the political will to push privatization could evaporate.

The Bottom Line

Ackman has described this as potentially generating more than $300 billion in additional profit for the U.S. government Stocktwits — which means this is a trade where the government’s interest and shareholders’ interests are aligned. That’s rare. Treasury Secretary Bessent has described a potential partial sale as “one of the biggest deals, maybe the biggest deal in history.” FHFA Director Bill Pulte’s fingerprints are on every Freddie earnings call.

The market is treating FNMA and FMCC as stranded assets in permanent bureaucratic limbo. The capital math, the management language, the political alignment, and now the loudest voices in contrarian investing are all pointing the same direction.

Ackman said it best: asymmetry at its best. The option value of privatization is currently priced at zero. The probability is not zero.

Disclaimer: Positions and price levels current as of March 30, 2026. This is not investment advice. Do your own due diligence.