Monitoring the Situation: The Iran Trade

"Good Progress" But Still Far Apart

"Even if nothing comes of Iran, oil and Brent are being repriced to our current geopolitical reality. They've been severely underpriced for months — the market is just now catching up to what the tankers already knew." — quantLR, LRMI

The Setup: Two Signals Before Breakfast

It started with a tweet.

Osint613 posted a flight radar map showing wall-to-wall tanker traffic streaming across the North Atlantic toward Europe and the Middle East. 3.2 million views.

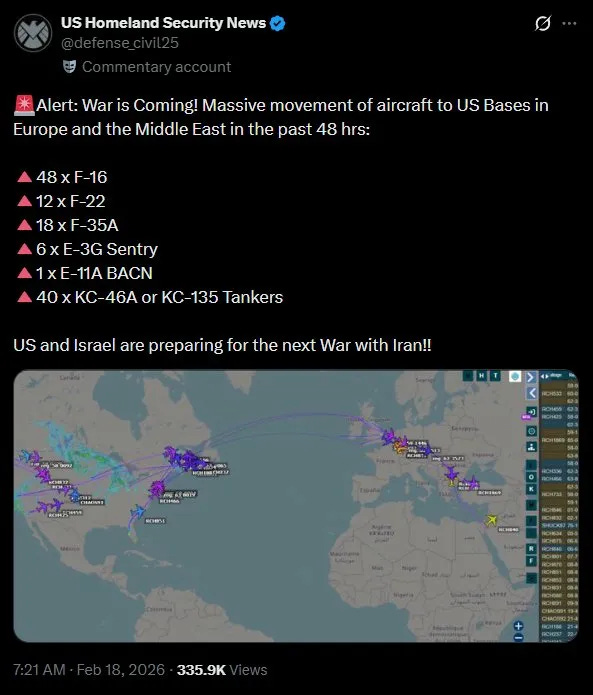

Then a second account — defense_civil25 — catalogued the specific assets moving in the last 48 hours:

48 x F-16s

12 x F-22s

18 x F-35As

6 x E-3G Sentry (airborne command and control)

1 x E-11A BACN (battlefield networking)

40 x KC-46A or KC-135 tankers

Two independent OSINT sources, same picture, within two hours of each other.

The F-22 deployment is the tell.

F-22s are pure air superiority aircraft. They don’t get deployed for “presence” or signaling missions. They get deployed when the US intends to fight for air dominance. Combined with 40+ tankers — the refueling architecture of a sustained, weeks-long campaign — this is a categorically different military posture than June 2025’s Midnight Hammer, which was a single night of B-2 sorties.

NBC News confirmed it: US military officials signaled all forces required for possible action would be in place by mid-March.

That date matters more than any diplomatic headline. I’ll explain why in a moment.

The Diplomatic Theater

Geneva talks wrapped Tuesday. Here’s how both sides spun the same meeting:

Iran (Araghchi): “Good progress. We agreed on guiding principles. We now have a clear path ahead.”

White House (Leavitt): “A little progress. We’re still very far apart on some issues.”

Classic negotiating optics. But here’s the detail that matters: on February 17th — the day before Araghchi’s “good progress” comments — Supreme Leader Khamenei delivered a speech explicitly stating Iran would continue uranium enrichment, would not negotiate on its missile program, and would not accept foreign demands.

Araghchi can sign any framework he wants. Khamenei controls the outcome.

Foreign Policy’s analysis said it best:

“If Tehran believes it can prolong negotiations toward US midterm elections to gain leverage, that would be a serious miscalculation. Washington’s tolerance for delay may expire long before any diplomatic timeline Tehran considers realistic.”

Iran is playing the long game. Trump is not. That mismatch is what makes a strike more likely than the “good progress” headlines suggest.

And the Polymarket crowd agrees. The “US Strikes Iran by March 31” contract sits at 64% with $10.9M in volume. That’s the market’s best guess at a coin-flip-plus for a strike before quarter-end.

What The Bloomberg Terminal Is Actually Showing

This is where it gets interesting. I spent the afternoon yesterday pulling every relevant data series I could find. Here’s what the institutional-grade data tells you that Twitter cannot.

*Data was obtained on 2/18 — 3:00 PM EST*

Signal 1: WTI Price — The Historical Analog

WTI was currently at $65.11, up $2.78 on the session. The June 2025 Midnight Hammer strike took crude from roughly $62 to a high of $75.14 in a matter of days. From current levels, that same magnitude move implies a run to the $76–78 range in a strike scenario.

The key observation: the December 2025 lows near $55 held, and crude is now building a base. Open interest is elevated and rising — new money is entering.

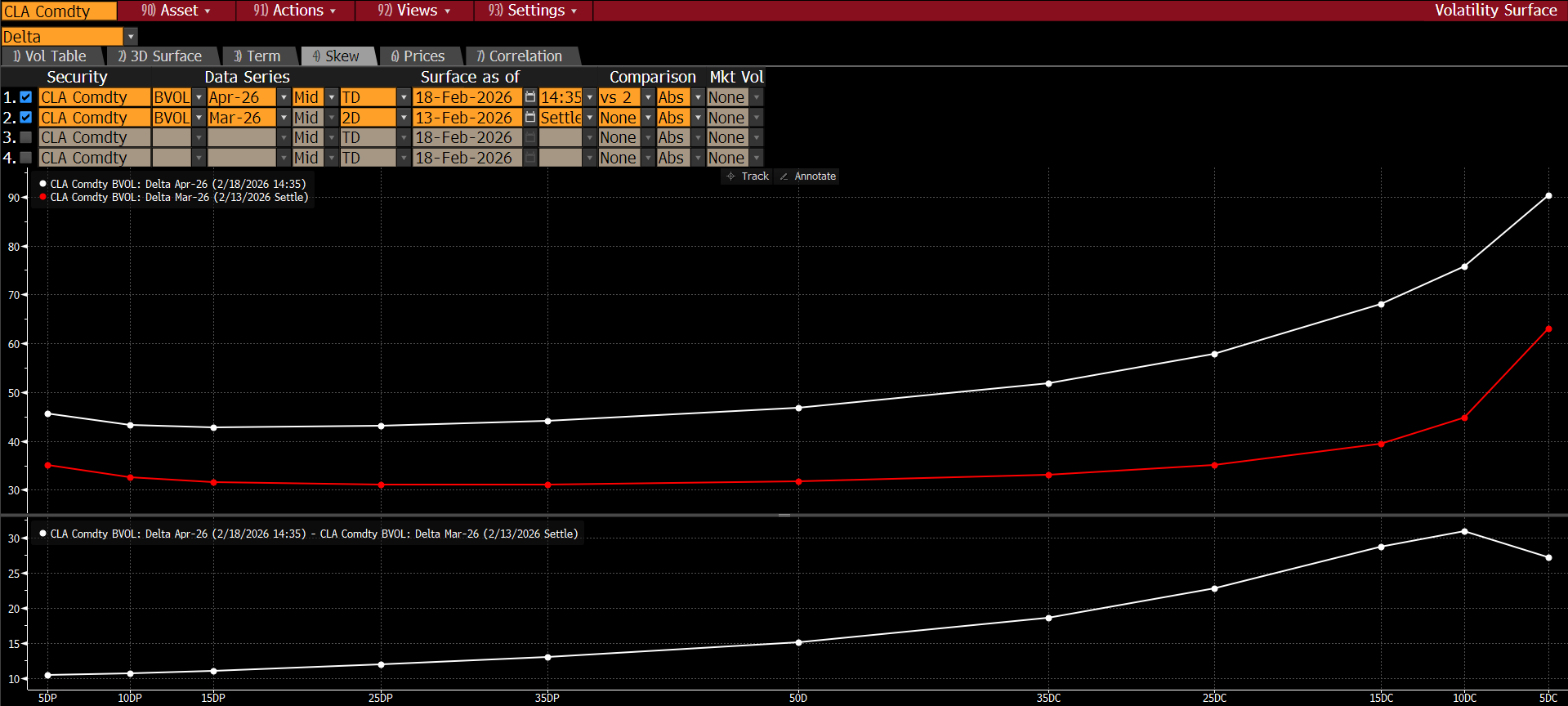

Signal 2: The Skew — This Is The Edge

This chart is the most important data point in my entire deck.

In the last five trading days, the April 2026 crude call skew has blown out dramatically versus where it was. Here’s what I’m seeing:

15-delta calls (deeply out-of-the-money options that only pay in extreme scenarios) are trading near 90 implied volatility

ATM vol is staying contained — meaning this isn’t general panic, it’s surgical

The differential between today’s skew and last week’s settle has expanded by 25–30 vol points at the call wing

When the call wing blows out while ATM vol stays stable, it means professional desks are buying upside protection on a specific tail scenario — not retail chasing. These are institutions making a deliberate bet, and they’re doing it quietly before mainstream financial media connects the dots.

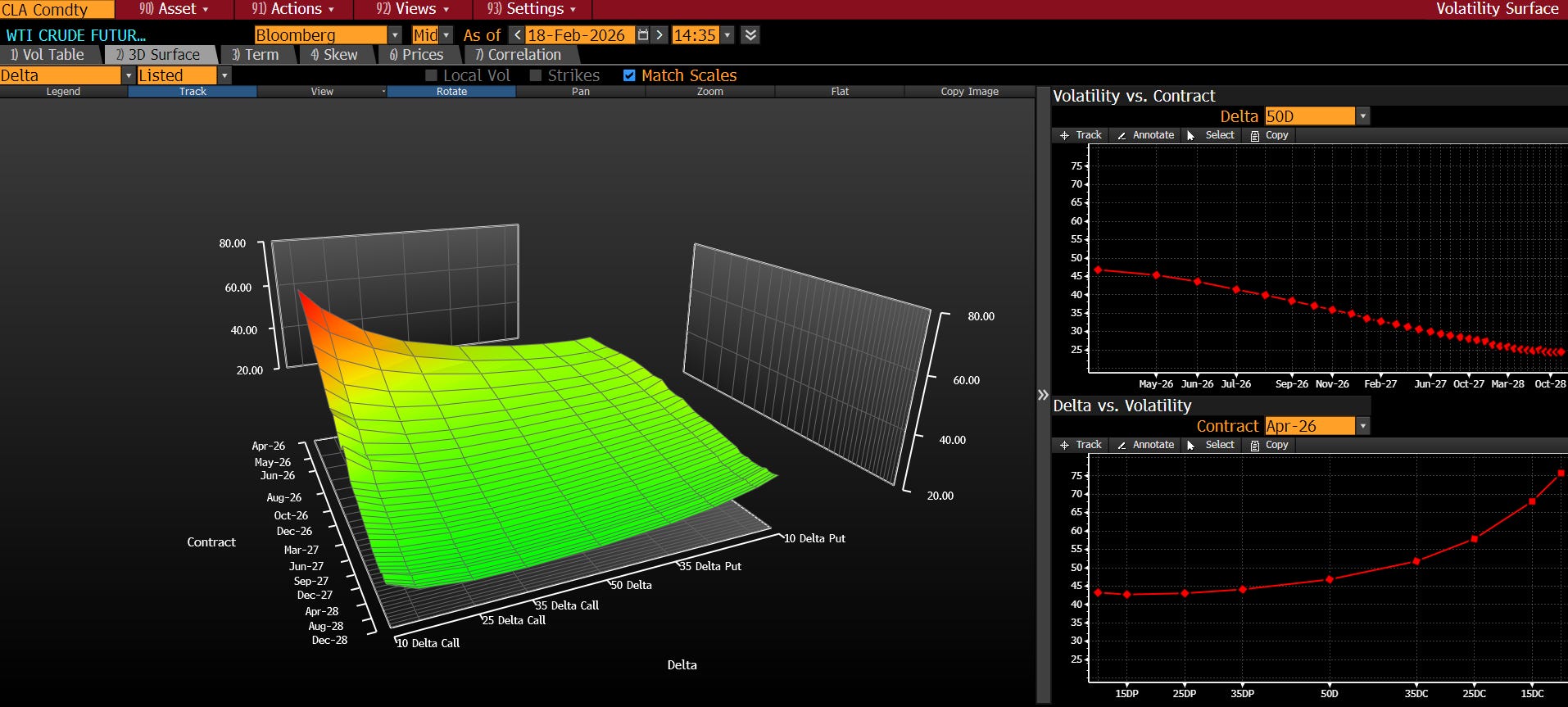

Signal 3: The 3D Volatility Surface

The 3D vol surface makes the same point visually. The front end — April 2026 — is the hot orange and red zone. The back end of the curve is flat green.

Near-term vol is dramatically elevated relative to longer-dated vol, meaning the market is pricing a near-term binary event, not a structural shift in the energy complex.

Signal 4: The Prompt Spread — The Futures Market Hasn’t Priced This Yet

The CL1-CL2 prompt spread is currently $0.14 — near the lows of the past year.

During June 2025’s Midnight Hammer operation, this spread spiked to $1.69 — a 12x move from current levels.

This is the asymmetry that makes the trade compelling:

Options market: Screaming danger (skew at multi-month highs, OVX at 51)

Futures market: Whispering calm (prompt spread nearly flat)

These two markets cannot stay diverged indefinitely. When the physical market catches up to the options market, it happens fast and violently. That gap closing is the catalyst that turns a good position into an exceptional one.

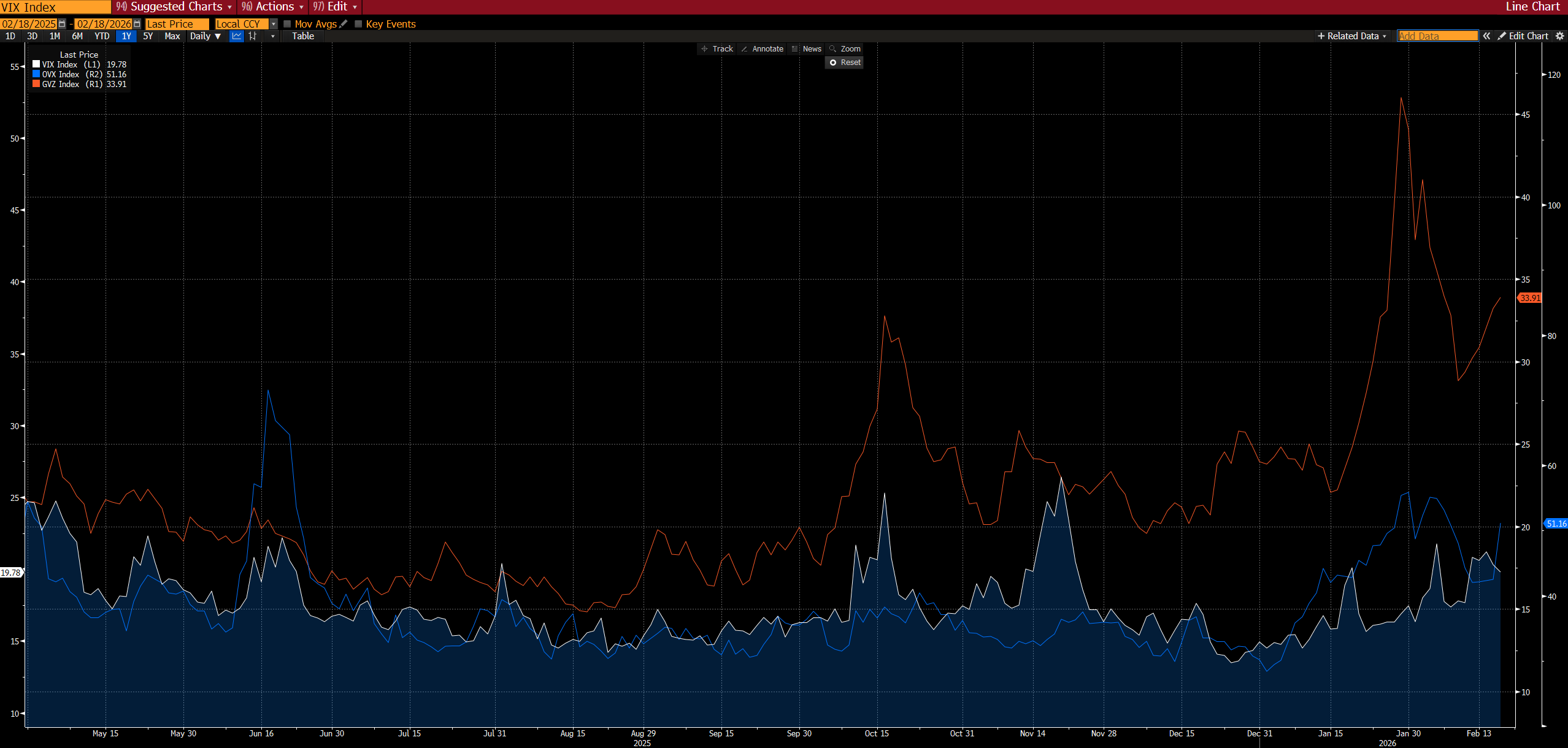

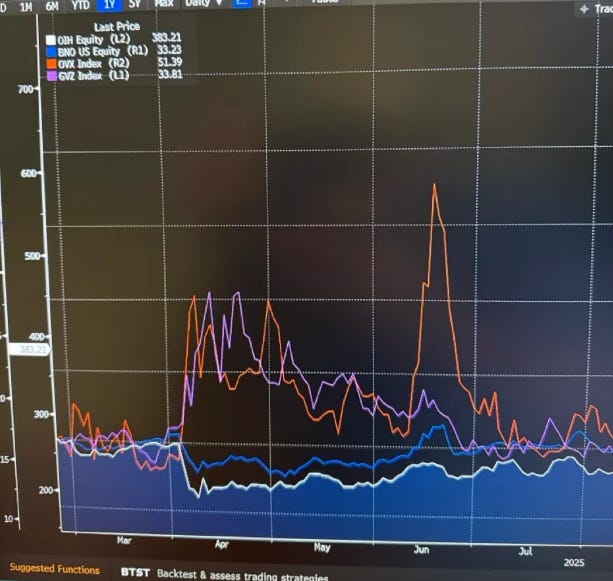

Signal 5: VIX vs OVX vs GVZ — The Divergence That Matters Most

VIX (equity vol): 19.78 — going DOWN

OVX (crude vol): 51.16 — going UP

GVZ (gold vol): 33.91 — going UP

This is the single most important chart in the deck. Equity traders are relaxed. Energy and gold traders are scared. The divergence is surgical — someone is hedging a specific geopolitical scenario, not a broad market crash.

The late January spike on this chart? That corresponded exactly to the peak Iran escalation moment when tensions surged before the first round of Oman talks. We’re building back toward that configuration right now, from a higher base.

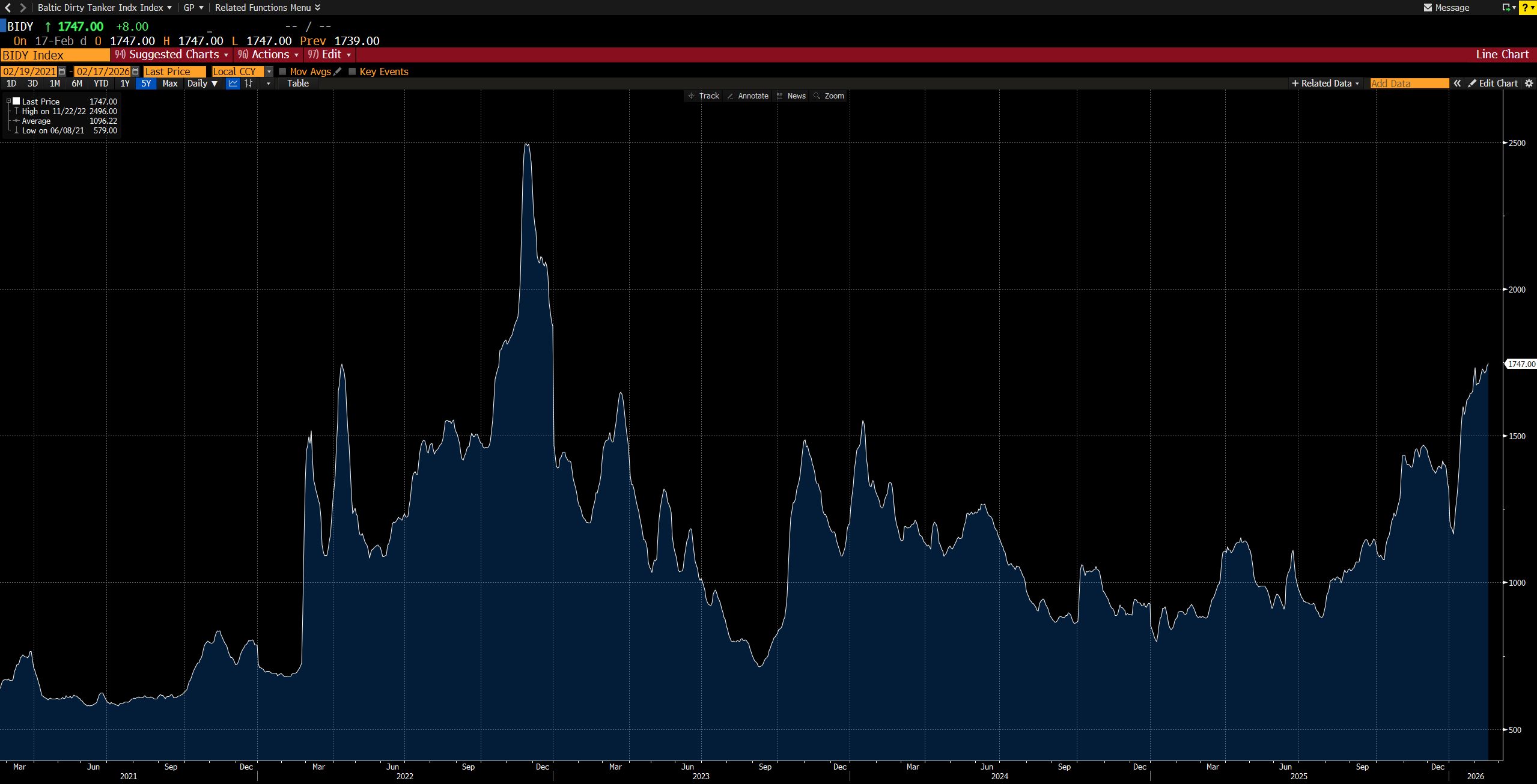

Signal 6: Baltic Dirty Tanker Index — 5-Year High

The BIDY is at 1,747 — near the highest levels since the 2022 Ukraine energy crisis.

Tanker rates don’t lie. Shipping companies price Hormuz risk in real time because their vessels are literally in the water. Here’s the divergence:

Tanker rates: 5-year highs — screaming supply disruption fears

WTI prompt spread: Nearly flat — priced for calm

This gap closes when it closes. It’s never gradual.

Signal 7: The Historical Playbook — June 2025

This overlay chart is the entire thesis in picture form. Look at what happened in the weeks before June 2025’s Midnight Hammer strikes:

OVX (crude vol) front-ran everything — it spiked first, before any price move

GVZ (gold vol) also led — smart money buying gold protection

OIH and BNO lagged — they moved hard after the vol signal was already established

Right now, OVX is at 51 and rising. GVZ is at 34 and rising. OIH and BNO haven’t exploded yet.

We are in Step 1 of a sequence that, last time, ended with oil services and Brent ETFs making generational moves.

Signal 8: Israeli Market — A Useful Barometer

The TA-35 closed up +0.87% yesterday. Israeli markets are not selling off.

This tells you something important: the people closest to this situation — Israeli traders with access to government intelligence flow and proximity to the conflict — are not pricing in an out-of-control escalation. They’re pricing either a clean deal or a swift, contained strike followed by a limited Iranian response.

Watch for the TA-35 to roll over. That’s your early warning signal that something went wrong in the next round of negotiations.

The BNO Options Flow That Caught My Attention

Yesterday’s session call volume on BNO: 1,542 contracts. Current session put volume: 31 contracts.

That is a 50-to-1 call/put ratio.

5-day average call volume: 770 — today ran at 2x the recent pace

20-day average put volume: 69 — today barely hit 31

Total call open interest: 12,994 vs. 1,696 puts — 88% of all open interest is call-side

Buried in the individual prints: 1,575 contracts of BNO February 35 calls — expiring this Friday — were bought in a single session. Someone spent roughly $15,000 on a 2-day lottery ticket that only pays if Brent rips more than 5% on a headline. They either know something, or they’re very convinced they’re right about the direction.

The Positions

Given everything above, here is how I’m thinking about this. The thesis has two legs — a sustained-conflict expression and a pure Brent spot expression. They’re complementary, not redundant.

OIH Mar 20 C400 — Oil Services, Sustained Conflict Expression

OIH at $383.80 at entry, strike $400, ~30 DTE

Oil services companies benefit from elevated crude prices over weeks and months, not just the initial spike

In a prolonged conflict scenario, capex returns to the energy sector and OIH re-rates

BNO Mar C35 — Pure Brent, Fast Money Expression

BNO at $33.21 at entry, strike $35

If a strike is announced, Brent front-runs every other instrument

In June 2025, BNO outperformed OIH on a percentage basis in the first 48 hours

50-to-1 call/put flow confirms institutional conviction on this name

These two positions together cover both the fast-money outcome (BNO wins on the initial spike headline) and the slow-money outcome (OIH wins in a prolonged conflict with sustained energy sector re-rating).

Pre-Market: February 19, 2026

Both moving in the right direction before the open. Both spiked up.

BNO 0.00%↑ outperforming OIH 0.00%↑ at 2.16% vs 1.00% pre-market is exactly what the June 2025 playbook predicted — Brent moves first, hardest, on the initial bid.

OIH’s C400 strike is now $11 away. One more strong session gets to $395 where delta accelerates sharply.

What I’m Watching This Week

Bullish continuation signals:

OVX continues rising above 55

GVZ pushes above 36

BIDY holds 5-year highs

CL1-CL2 prompt spread begins moving — this is the critical confirmation that the physical market is catching up to the options market

USD/ILS (shekel) weakens — Israeli FX is the fastest real-time geopolitical stress gauge available

Iran’s written proposals to the US come back weak or are publicly contradicted by Khamenei

Exit / stop signals:

OVX compresses back below 45 while BIDY simultaneously rolls over — the institutional bid is fading, exit regardless of headlines

Geneva talks produce a credible written framework with Khamenei explicitly endorsing it — deal thesis takes over

TA-35 starts selling off while everything else holds — suggests a rogue escalation scenario the market isn’t pricing correctly

The binary resolution window:

Iran offered to return with detailed proposals “within two weeks.” The US military will be fully positioned by mid-March. My March 20 expiries sit inside that window almost exactly. This isn’t a coincidence — it’s the market’s built-in timer on this trade.

The Bottom Line

Every data series is telling the same story and it’s coherent:

The options market is leading the futures market. The crude skew has blown out. OVX is diverging from VIX. Tanker rates are at 5-year highs. BNO call flow is running 50-to-1. And yet the WTI prompt spread is flat and LMT/ITA defense vol is still cheap.

The window between institutional positioning and mainstream financial media catching on is typically 24–48 hours. We appear to be inside that window right now.

Iran thinks it’s playing the long game. The US military just told us it will be ready to act by mid-March. My options expire March 20.

The trade has a timer built in. And it’s running.

Disclaimer: Not investment advice. Options trading involves substantial risk of loss including total loss of premium paid. Do your own due diligence before trading any instrument mentioned. Past performance is not indicative of future results.