Is Micron Having Its “NVIDIA Moment”?

AI Demand, Sold-Out Supply, and Why Memory Is Being Repriced as Infrastructure

For most of the last decade, memory was treated as a commodity — cyclical, price-sensitive, and structurally inferior to compute.

AI has quietly broken that framework.

Micron MU 0.00%↑ is now posting numbers that look uncomfortably similar to NVIDIA NVDA 0.00%↑ in mid-2023, right before the market repriced it as a foundational AI infrastructure company.

The question isn’t whether Micron benefits from AI.

The question is whether the market is still anchoring to an obsolete mental model.

The inflection looks familiar

NVIDIA’s re-rating didn’t start with hype — it started with three hard signals:

Revenue reached infrastructure scale

Margins expanded beyond historical ceilings

Supply sold out faster than it could be built

Micron now checks all three.

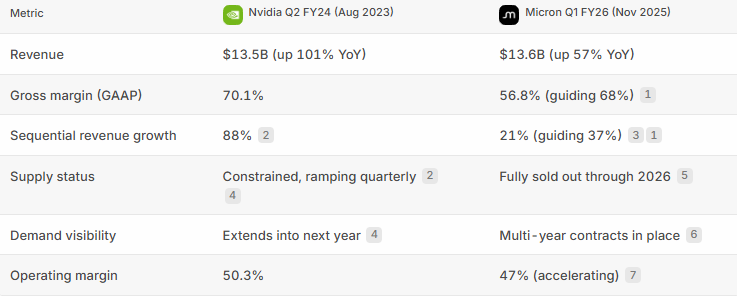

Revenue has crossed the same threshold

Micron Q1 FY26 revenue: $13.6B, up 57% YoY

NVIDIA’s breakout quarter (Q2 FY24): $13.5B, up 101% YoY

That similarity matters. Once revenue reaches this scale, incremental demand converts directly into earnings power, not just growth optics.

Micron is now guiding 37% sequential growth into Q2 FY26 — acceleration, not deceleration.

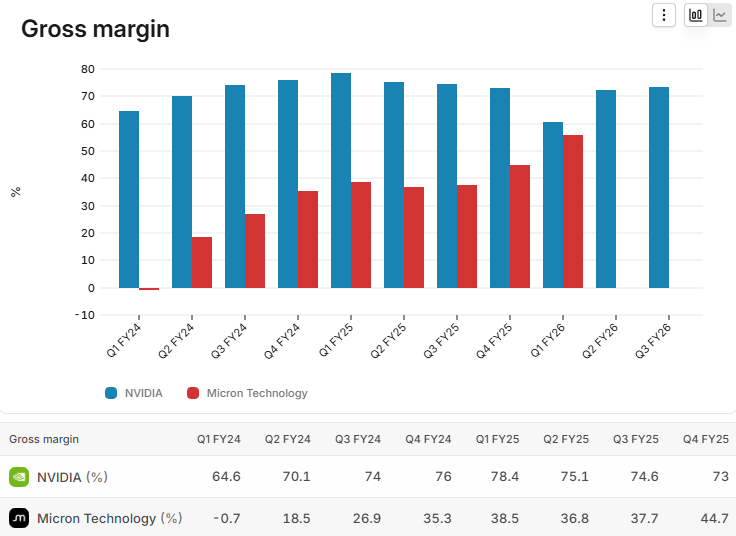

Margins are breaking historical ceilings

This is where the story changes.

Memory companies historically peaked in the 30–40% gross margin range before pricing collapsed.

Micron just printed 56.8% GAAP gross margins — and guided 68% next quarter, a level unprecedented in its history.

For context:

NVIDIA was at 70.1% gross margins during its inflection

NVIDIA’s multiple expanded before margins peaked

Margins later climbed toward ~78%

Micron isn’t late.

It’s early in the same margin expansion curve.

Supply is no longer elastic — it’s spoken for

The most underappreciated shift in memory is contract structure.

Micron’s HBM supply:

Fully sold out through calendar 2026

Backed by multi-year customer agreements

Industry-wide shortages in DRAM and NAND, not just Micron-specific

This mirrors NVIDIA’s 2023 setup — except with longer duration visibility.

When supply is pre-sold, revenue volatility collapses.

Execution replaces speculation.

Memory has moved from component → strategic bottleneck

Micron’s relationship with NVIDIA isn’t incidental.

They:

Co-developed LPDRAM for servers

Built SOCAMM modules for GB300

Have SSDs approved for NVIDIA’s GB200 platform

This matters because HBM is now a system-level constraint, not a swappable input.

The HBM total addressable market is now projected to reach $100B by 2028, pulled forward two years.

That acceleration didn’t happen in smartphones or PCs — it happened in AI factories.

Memory density, latency, and power efficiency now determine system performance.

Operating leverage has arrived

Micron’s operating margin just reached 47%, with management explicitly stating it is still accelerating.

That puts Micron within striking distance of NVIDIA’s operating profile during its breakout — despite operating in what the market still labels a “commodity” segment.

Free cash flow margins are approaching 30%, even as Micron aggressively expands capacity.

This is not a late-cycle squeeze.

This is structural operating leverage.

The valuation disconnect

Here’s the part that doesn’t reconcile.

Micron today has:

50%+ revenue growth

Gross margins expanding toward ~70%

Sold-out supply through 2026

Multi-year AI-linked contracts

Operating margins nearing 50%

And trades at a single-digit forward P/E.

At the same stage:

NVIDIA carried a premium multiple

The market assumed durability far earlier

The only reason for this gap is anchoring — investors are still pricing Micron as a cyclical memory producer, not an AI infrastructure bottleneck.

What this actually is (and what it isn’t)

Micron is not “the NVIDIA of memory.”

It is something more precise:

The first memory company whose economics are being structurally reshaped by AI infrastructure demand.

That distinction matters.

Platforms get recognized early

Critical enablers get repriced late

If this were just a cyclical upswing, margins wouldn’t be resetting at historic highs, contracts wouldn’t extend years forward, and customers wouldn’t be fighting for allocation.

Bottom line

Micron now exhibits the same fundamental signals NVIDIA showed at its moment:

Infrastructure-scale revenue

Margin inflection beyond historical ceilings

Sold-out supply with expanding demand visibility

Rapid operating leverage

Yet the market is still using old memory playbooks.

That mismatch doesn’t persist indefinitely.

Disclosure: This is not investment advice. This is for research purposes only.

CVX and XOM Just Did Something That Happens Once Every 55 Years

“You got a death wish, or is this a business decision?”

Like your work!