Intel Q1 2026 Earnings

Analyzing Intel's Q1 '26 Earnings

High-Level Read

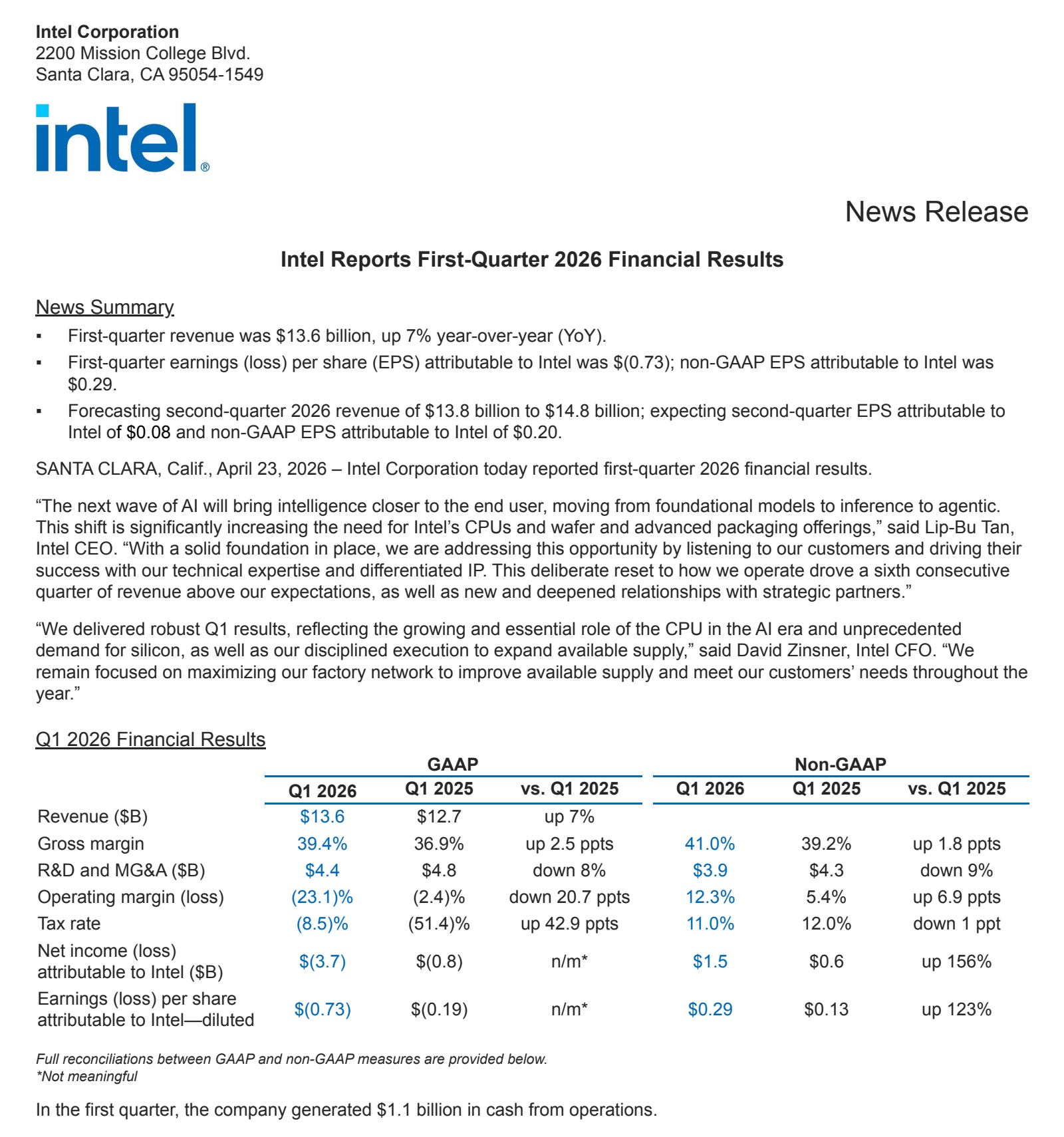

INTC 0.00%↑ Intel delivered its sixth consecutive quarter beating expectations, with Q1 2026 revenue of $13.6 billion, up 7% YoY.

The beat was broad-based — revenue came in$1.4 billion above the midpoint of guidance, driven by supply improvements, better mix, and pricing actions.

The GAAP loss was distorted by a $3.9 billion non-cash goodwill impairment charge on Mobileye, driven by increased discount rates and macro uncertainty — not an operational deterioration. AI-driven businesses now represent 60% of revenue and grew 40% YoY!

Q2 2026 guidance: Revenue of $13.8–$14.8 billion, non-GAAP gross margin of 39.0%, non-GAAP EPS of $0.20. DCAI guided to grow double digits sequentially.

LRMI: Analysis: Data Center & AI Infrastructure Demand

I believe this is where the real signal is. Management was unusually direct about a structural shift in the CPU-to-accelerator compute ratio, and the data center numbers confirm it.

DCAI Segment — The Core Thesis

DCAI revenue: $5.1 billion, up 22% YoY and 7% sequentially, described as “well above expectations.”

ASIC revenue nearly doubled YoY and was up >30% sequentially — an underappreciated growth vector.

Operating profit: $1.5 billion at 31% margin, up ~$292M QoQ on better yields and cycle times on Intel 3.

The CPU-to-GPU Ratio Inflection — The Most Important Data Point on the Call

Management quantified what the market has debated: the ratio of CPUs to GPUs in AI workloads is structurally shifting toward CPUs as AI matures:

Training: ~7–8 GPUs per 1 CPU

Inference: now closer to 3–4:1

Agentic / multi-agent: approaching parity or better for CPUs

CEO Lip-Bu Tan reinforced this: “The backbone of AI computing in production remains a CPU-anchored architecture... CPU is the orchestration layer and critical control plane for the entire AI stack.”

Inference requires CPU-heavy orchestration for managing multi-agent data flows where power-per-performance matters.

Demand Signals Are Getting Stronger, Not Weaker

Server CPU unit TAM outlook improved over the last 90 days — Intel now expects double-digit unit growth for the industry and for itself, with momentum extending into 2027.

Supply, not demand, is the binding constraint. Management explicitly stated demand continues to outpace their growing supply.

To address this, tool spending is increasing ~25% YoY even as total CapEx stays flat — a signal of deliberate capacity acceleration on the manufacturing side.

Customer Wins — Structural, Not Transactional

Google signed a multi-year long-term supply agreement for Xeon IPU in Q1, with Lip-Bu describing it as a “long-term trusted partnership.” More contracts to be announced.

NVIDIA’s DGX Rubin NVL8 selected Xeon 6 as the host CPU — Intel is embedded in the most advanced AI training systems being shipped today.

SambaNova signed a multiyear collaboration for next-gen heterogeneous AI inference architectures combining SambaNova RDUs with Xeon 6.

Advanced Packaging — A Scarce and Strategic Asset

The semiconductor TAM is approaching $1 trillion driven by AI demand. Intel has identified three strategic moats: the x86 CPU franchise, advanced packaging, and the manufacturing network.

Advanced wafer and packaging capacity remains inshort supply industry-wide, which benefits Intel’s vertically integrated supply chain. The company is expanding its back-end facilities in Penang, Malaysia on a multi-year horizon.

Near-Term Gross Margin Watch

CFO Zinsner flagged that Q2 gross margin will step down from 41% to 39% due to Panther Lake (18A) volume ramping ~6–7x QoQ — still below corporate average margins. Input cost inflation (substrates, T-glass, memory) is also a headwind in H2. This is a ramp tax, not a demand problem.

Stanley Druckenmiller Variant Perception

Using Druckenmiller’s framework: find the consensus that is wrong, identify the leading indicator the market is missing, and size the bet on the rate of change, not the level.

What the Market Has Wrong

The market’s dominant narrative has been “GPU wins AI, CPU is commoditized legacy silicon.” Intel has traded as a restructuring story, not a growth story. The variant perception emerging from this call is that this framing is 3 years stale.

The Asymmetric Setup

The CPU TAM is being re-rated in real time. The market modeled GPU/accelerator-centric AI infrastructure. The shift to inference and agentic AI is a second derivative change that dramatically increases CPU intensity per unit of compute output. Intel’s own numbers — DCAI +22% YoY, server CPU TAM now expected up double-digits vs. flat expectations 90 days ago — are the leading indicator. The rate of change in estimates is what Druckenmiller would focus on.

Supply is the constraint, not demand. When demand exceeds supply and the company is accelerating tool spend 25% YoY, you have a pricing power and revenue upside setup into H2 and 2027. The market is discounting Intel on margin concerns (18A ramp costs) without properly crediting the demand backlog building underneath.

18A is a free call option the market is not pricing. Yields are running ahead of internal projections — described as a “meaningful inflection.” If 18A yields continue to improve and external foundry customers commit (Intel has flagged that 14A continuation depends on external design wins), Intel goes from a one-asset story (x86 CPUs) to a two-asset story (x86 + foundry), re-rating the stock.

Intel 18A The ASIC business is hiding in plain sight. ASIC revenue nearly doubled YoY and grew 30%+ sequentially. This is structurally attached to the custom silicon wave (hyperscalers building their own chips). Intel’s packaging and manufacturing capabilities make it a natural beneficiary. The street is not modeling this segment discretely.

Consensus is modeling PC weakness as a drag. Full-year PC TAM is expected down low double digits and H2 client is weak. This is the consensus anchor weighing on Intel’s multiple. But CCG is now >60% AI PC mix. As AI PC penetration grows and the platform refreshes, the downside case on CCG may be more muted than feared.

The Risk That Kills the Variant View

The bear case is straightforward: 18A fails to attract sufficient external design wins, making the foundry investment a value destroyer with no revenue to justify it. Management explicitly flagged that 14A development could be paused if external customer demand isn’t secured.

Additionally, input cost inflation (substrates, memory, helium shortages) compressing margins in H2 could cause estimate cuts that overshadow the demand recovery narrative. The bet requiresprocess execution— which Intel has historically struggled to deliver on time.

Bottom line: The earnings call revealed a company where the demand picture is materially better than expected and improving, the CPU structural narrative is gaining real-world confirmation, and the primary risk is self-inflicted execution (18A ramp, costs) rather than market demand. The variant perception is that Intel is being priced as a restructuring story when the data now supports framing it as an AI infrastructure beneficiary in an early innings re-rating.

With CPU plays like INTC 0.00%↑, AMD 0.00%↑, and ARM 0.00%↑ surging +40% in just two weeks, it’s clear the market is aggressively correcting a previous mispricing in the space. I anticipate a rotation of profits back into GPU leaders like NVDA 0.00%↑, whose May 20 earnings (T-24 days) will serve as a definitive litmus test for both GPU demand and the broader AI sector.

Disclaimer: This is for Educational purposes only. Not a solicitation to buy or sell securities. NFA.