Everyone's Watching Mortgages. Nobody's Watching the Car Loans.

A forensic deep dive into Ally Financial — the largest pure-play auto lender in America — and why its balance sheet rhymes with patterns that ended badly before in 2008.

I Went Car Shopping with My Parents

I was at the dealership with my parents last week. My parents both have 800+ credit scores, as clean as it gets. The salesman rattled off the banks they use for financing: Chase, BofA, and Ally. Chase won the rate, but the name "Ally" stuck with me. Because I know something most car buyers don't.

Ally Financial isn’t a diversified bank. It’s a car loan company that happens to have a banking charter. Roughly 59% of its total assets — about $115 billion — are tied directly to auto lending. The vast majority of its revenue and profit come from one thing: Americans making monthly payments on their cars.

And that got me thinking. In 2008, the biggest liability most Americans held was a mortgage. The second biggest? A car loan. If there’s another recession → a real one, with unemployment spiking and consumers stretched thin — the company most exposed to that second-biggest liability is Ally ALLY 0.00%↑.

So I went digging. I used Quartr AI to pull every earnings transcript, every slide deck, every management admission from the past three years. What I found was — frankly — remarkable.

Here’s the full forensic breakdown.

The Macro Setup: America's Auto Debt Problem

Before we even touch Ally’s filings, look at what’s happening to American car buyers right now.

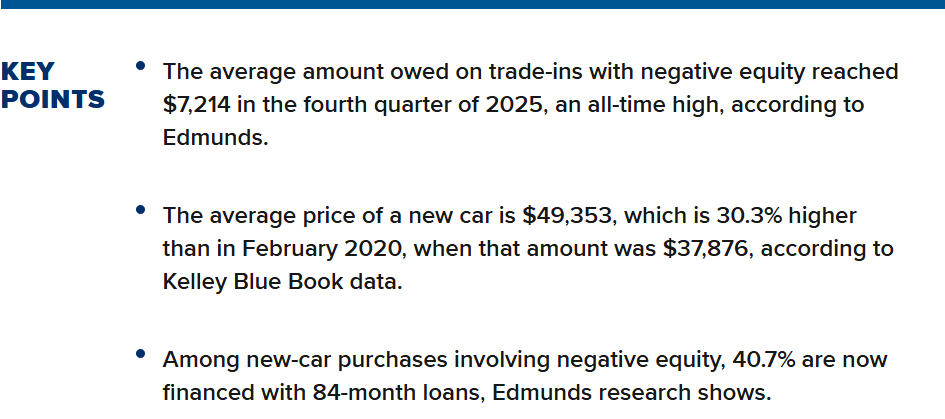

30.5% of car buyers trading in a vehicle are underwater — they owe more than the car is worth. That’s up 4.2 percentage points from a year ago (JD Power, March 2026).

The average amount of negative equity hit an all-time record of $7,214. The average monthly payment for these underwater buyers is $916. And 40.7% of them are on 84-month (7-year) loans just to afford the payment.

The average new car now costs $49,353 — up 30% from 2020. Americans owe $1.7 trillion in total auto debt. And many of the cars being traded in underwater were purchased during 2022–2023, when prices were at their absolute peak.

This is the consumer environment Ally Financial operates in. Now let’s look inside.

Next is my research from Quartr:

Red Flag #1: The Asset-Liability Time Bomb

This is the structural flaw at the center of everything. Michael Burry’s key insight in 2005 was that mortgage lenders had locked in long-duration fixed-rate income but funded themselves with short-duration, rate-sensitive liabilities. Ally has the exact same architecture — just in auto! Literally holy smokes!

Ally’s consumer auto portfolio is fixed-rate — loans originated at whatever rate was set, locked in for 5–6 years. But Ally funds itself primarily with floating-rate deposits (high-yield savings, money markets) that reprice immediately when rates move.